Free Practice Questions for the ACI-Financial 3I0-012 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the ACI 3I0-012 exam. To support your certification journey, we have made a selection of our premium 2026 ACI-Financial practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

What does the Model Code recommend with regard to any give-up agreement between a prime broker and an executing dealer?

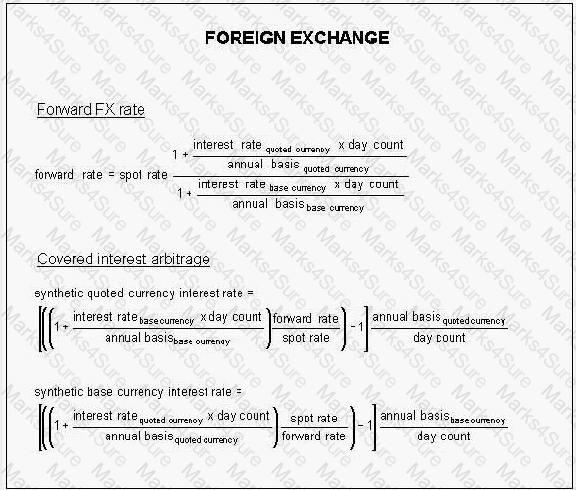

If EUR/USD is quoted to you as 1.3030-40 and GBP/USD as 1.5320-30, at what rate can you sell GBP and buy EUR?

Which of the following statements reflects the Model Code on gambling or betting amongst market participants?

When an employee executes a personal trade in advance of a client’s or institution’s order to benefit from the anticipated movement in the market price following the execution of a large trade, it is called:

The one-month (31-day) GC repo rate for French government bonds is quoted to you at 3.75-80%. As collateral, you are offered EUR25 million nominal of the 5.5% OAT April 2006, which is worth EUR 28,137,500. If you impose an initial margin of 1%, the Repurchase Price is:

How many USD would you have to invest at 3.5% to be repaid USD125 million (principal plus interest) in 30 days?

If you sell USD 3-month forward to a client against EUR, what should you do to hedge your position?

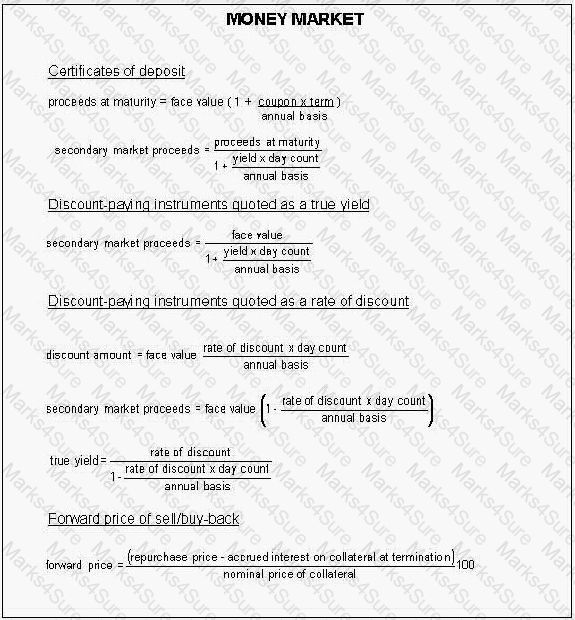

A 3-month (91-day) US Treasury bill is quoted at a rate of discount of 4.25%. What is its true yield?

In the event that standard settlement instructions are provided by a third party, full authentication and authorization of those SSIs should be independently performed by?

The primary issue for insuring prudent liquidity management in accord with the guidance provided by the Basel Committee (Basel II I Basel III) is:

A transaction that entails market price risks may be entered into in the absence of a market price risk limit...

You are short of 6 December EURODOLLAR futures contracts at 99.50. Yesterday, the closing price was 99.35. Today’s closing price is 99.105. What variation margin will be due?

Which of the following both provide credit enhancement to a true-sale securitization?

All other things being equal, if a bank borrows short and lends long what is the effect on the liquidity risk of the bank?

What should be done when a voice broker calls “off” at the very instant the dealer hits the broker’s price as “mine” or “yours”?

You are quoted the following rates:

Spot cable 1.5340-43

0/N cable swap 0.14/0.11

T/N cable swap 0.16/0.13

S/N cable swap 0.43/0.37

At what rate can you buy cable for value tomorrow?

The 180-day CAD/CHF rate is bid 62 and the 90-day CAD/CHF rate is bid 29. What is the bid rate for 120 days, assuming straight-line interpolation?

Which of the following transactions would have the effect of shortening the average duration of liabilities in the banking book?

Under the Model Code, if a broker shouts “done” or “mine” at the very moment a dealer shouts “off”:

Your GBP/CHF rate is 1.3710-15. How many GBP would your customer have to give you to buy CHF 10,000,000.00?

Which of the following market participants would least likely be a user of repo?

What needs to be done in the event that a trade is amended by one or both parties?

If EUR/USD is 1.3025-28 and the 6-month swap is 15.50/17, what is the 6-month outright price?

What is the expression used to describe a genuine error (wrong amount, wrong side, wrong rate) made by a dealer in the execution of an order on an electronic platform?

A customer gives you GBP 25,000,000.00 at 0.625% same day for 7 days.

Through a broker, you place the funds with a bank for the same period at 0.6875%.

Brokerage is charged at 2 basis points per annum.

What is the net profit or loss on the deal?

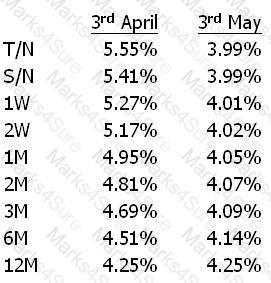

The columns below list short-term cash rates on 3rd April and 3rd F1ay 3rd April 3rd May

Describe the shape of the short-term segment of the yield curve on 3’ April using market terminology. In addition, describe the change in the shape of the curve between 3rd April and 3rd May.

If the issuer of the collateral used in a repo defaults during the term of the transaction, who suffers the loss?

At the end of the day, you are short CHF 3,500,000.00 against SEK at 6.9275. You are asked to revalue your position at 6.9190. What is the resulting profit or loss?

Which one of the following statements about mark-to-model valuation is correct?

You and a dealer at another bank have a verbal bilateral reciprocal arrangement to quote each other two-way prices. During periods of high volatility, the other dealer refuses to quote to you. What does the Model Code say about this situation?

Claims should be communicated in writing via e-mail or preferably by authenticated SWIFT. What information should be provided in the claim?

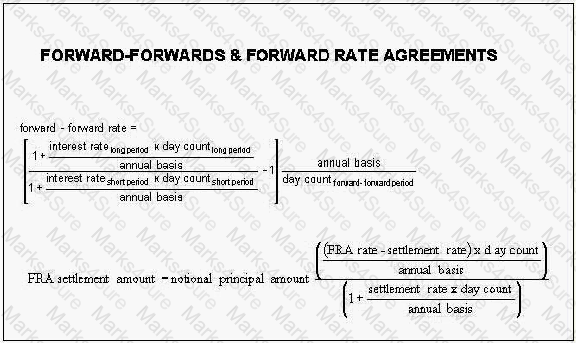

A 3-month (90-day) NZD deposit is 2.75% and 6-month (180-day) NZD deposit is 3.00%. What is the 3x6 NZD deposit rate?

Where voicemail equipment is used for the reporting and recording of off-premises transactions, voice mail should be:

What does the Model Code recommend in respect of prices and orders made on electronic trading platforms?

How many Yen would you pay to buy 1 ounce of gold if you were quoted the following?

XAU/USD 1575.25-75

USD/JPY 96.55-60

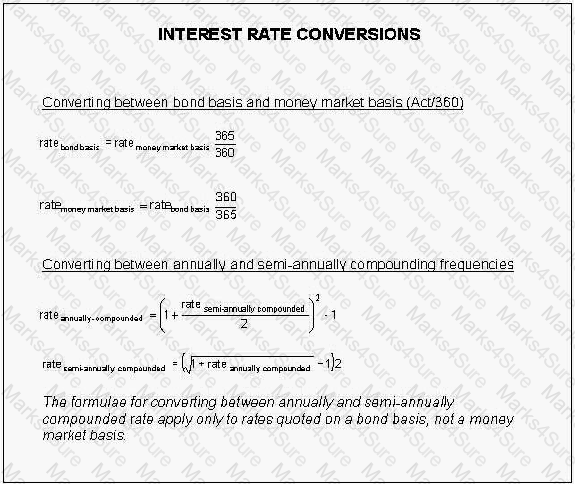

Which of the following currencies is quoted on an ACT/365 basis for the calculation of interest on interbank deposits in London?

The Model Code recommends that standard terms and conditions be used in legal documents. Which one of the following statements is correct?

What does the Model Code say about omitting the “big figure” in voice communication?

A CD with a face value of USD 250,000,000.00 was issued at par with a coupon of 5% for 91 days.

You buy it in the secondary market when it has 30 days remaining to maturity and is trading at

5.25%. How much do you pay?

The Interest Rate Parity Theorem should work because, when one sells a low interest rate currency to invest in a high interest rate currency and hedges the currency risk:

You are a sales person in a bank and are about to sell a structured note to a non-professional customer. Before finalizing the transaction you remember to double-check the customer’s charter. You learn that the customer is not allowed to invest in structured products. The risk you have avoided is most likely to be classified as:

The Model Code stipulates that you have a right to qualify your quotes in terms of amounts:

You are the buyer of a receiver’s swap. All other things being equal your counterparty risk is increasing if

What is the result of combining a 1-month buy and sell FX swap with a 2-month sell and buy FX swap?

Responsibility for the activities of all personnel engaged in dealing (both dealers and support staff) for both principals and brokers lies with:

You have taken 3-month (92 days) deposits of CAD 12,000,000.00 at 1.10% and CAD 6,000,000.00 at 1.04%. Minutes later, you quote 3-month CAD 1.09-14% to another bank. The other dealer takes the CAD 18,000,000.00 at your quoted price. What is your profit or loss on this deal?

The mid-rate for USD/CHF is 0.9300 and the mid-rate for NZD/USD is 0.8560. What is the mid rate for NZD/CHF?

Where dealing for personal account is allowed, what safeguards to prevent abuse or insider dealing are stated by the Model Code?

You quote a customer a spot cable 1.6050-55 in USD 3,000,000.00. If they sell USD to you, how much GBP will you be short of?

Which of the following statements is true concerning dealing and rollovers at non-current rates?

Lending for 3 months and borrowing for 6 months creates a 3x6 forward-forward deposit. The cost of that deposit is called:

Which of the following does the Model Code mention with regards to recording telephone conversations?

Today’s spot value date is the 30th of June. What is the maturity date of a 2-month EUR deposit deal today? Assume no bank holidays.

Assuming a flat yield curve in both currencies, when quoting a 1- to 2-month forward FX time option price in a currency pair trading at a discount to a customer:

The use of standard settlement instructions (SSI’s) is strongly encouraged because:

What is the amount of the principal plus interest due at maturity on a 1-month (32-day) deposit of USD 50,000,000.00 placed at 0.37%?

In GBP/CHF, you are quoted the following prices by four different banks. You are a buyer of CHF. Which is the best quote for you?

You request use of funds from your agent bank for 1 day on an amount of EUR 100,000,000.00, EONIA was 0.812% and the ECB deposit facility rate is 0.50%. What use of funds settlement amount should you expect?

A 7% CD was issued at par, which you now purchase at 6.75%. You would expect to pay:

What is the correct interpretation of a EUR 2,000,000.00 overnight VaR figure with a 97% confidence level?

A euro zone-based bank that is asset-sensitive to market interest rate changes might reduce interest rate risk by:

The spot/week repo rate for the 4.25% OAT 2015 is quoted to you at 2.35-38%. You buy bonds with a market value of EUR 3,295,500.00 through a sell/buy-back. The Repurchase Price is:

3-month EUR/USD FX swaps are quoted to you at 8/12. If the “points are in your favor”, what have you done?

You buy a 30-day 4% CD with a face value of GBP 20,000,000.00 at par when it is issued. You sell it in the secondary market after 10 days at 4.05%.

What is your holding period yield?

A dealer has been invited by a broker to go to an exclusive club for the third time in a week. He should:

Which of the following are specifically quoted in terms of a yield-to-maturity?

You sold a JPY 500,000,000 1x12 FRA at 0.35%. The settlement rate is 11-month (334-day) JPY LIBOR, which is fixed at 0.4450%.

What is the settlement amount at maturity?

In interbank trading, if a dealer is calling “off” at the same time as the broker is hitting a price:

Spot EUR/USD is 1.3050-53 and EUR interest rates are lower than USD interest rates. Would you expect the forward points for EUR/USD to be:

You are quoted spot USD/NOK 5.7220-28 and USD/SEK 6.3850-58, at what price can you buy NOK against SEK?

A US security yields 7% on an annually-compounded bond basis. What is the equivalent annually- compounded money market yield?

If 6-month USD/CAD forward rates are quoted at 40/45, which of the following statements is correct?

In the international market, a FRA in USD is usually settled with reference to:

You are quoted the following rates:

Spot GBP/USD 1.5295-00

Spot USD/CHF 0.9320-23

6M GBP/USD swap 16/12

6M USD/CHF swap 22/18

Where can you buy GBP against CHF 6-month outright?

Repo is said to have “double indemnity” due to the creditworthiness of the counterparty and:

Which of the following statements about leverage ratios under Basel III is correct?

You are quoted the following rates:

Spot GBP/CHF 1.4535-45

3M GBP/CHF swap 22/19

At what rate can you sell GBP against CHF outright 3-month?

Where sale and repurchase agreements or stock borrowing or lending transactions are entered into:

You have done the following deals in spot USD/JPY:

Sold USD 5.0 million at 111.60

Bought USD 3.5 million at 111.20

Bought USD 2.0 million at 111.50

Sold USD 2.0 million at 111.55

What position do you now have?

You bought USD 5,000,000 against EUR at 1.1037 and 3,000,000 at 1.1052. If the EUR/USD rate is now quoted 1.1015/17, and it you deal at that rate, what profitwould you make?

When dealing with a fund manager, who will allocate shares in a transaction to his unknown clients after the transaction has been executed with you, you should:

Using the following rates:

3M (90-day) eurodeposits3.50%

6M (180-day) eurodeposits3.75%

What is the rate for a deposit, which runs from 3 to 6 months?

At the end of the day you are short EUR 10 million against GBP at 0.6712. You are asked to revalue your position at a EUR/GBP rate of 0.6729. What is the resulting profit or loss?

A CD with a face value of USD 50 million and a coupon of 4.50% was issued at par for 90 days and is now trading at 4.50% with 30 days remaining to maturity. What has been the capital gain or loss since issue?

You hear from several counterparties that a major market participant has taken major losses on long USD/JPY positions. You know the reports are untrue, as you have in fact bought large amounts of USD/JPY from that very firm, which means that the impact of the reports on the market would be helpful to your position.

A 3-month (91-day) deposit of EUR25 million is made at 3.25%. At maturity, it is rolled over three times at 3.55% for 90 days, 4.15% for 91 days and 4.19% for 89 days. At the end of 12 months, how much is repaid (principal plus interest)?

When quoting the exchange rate between the EUR and AUDI which is conventionally the base currency?

What does the Model Code say about the responsibility of a broker in handling suspicious transactions?

From the following GBP deposit rates:

1M (31-day) GBP deposits 3.15%

2M (61-day) GBP deposits 3.25%

3M (91-day) GBP deposits 3.41%

4M (120-day) GBP deposits 3.56%

5M (152-day) GBP deposits 3.73%

6M (182-day) GBP deposits 3.90%

calculate the 3x4 forward-forward rate.

When dealing with customers, financial market professionals are advised by the Model Code to clarify that all transactions are entered into solely at each partys risk by explicitly agreeing in writing that:

You have quoted a Swiss customer spot USD/CHF as 1.3710-15, but he asks you to quote it as CHF/USD. What do you quote?

Where dealing through an intermediary with an unidentified principal, the Model Code recommends:

A disgruntled customer claims that he should not have to settle an FRA with you because it is really just a wager. What type of risk are you exposed to?

A 7-day piece of USCP is quoted at a rate of discount of 1.75%. What is its true yield?

The organisational structure of market participants should ensure a strict segregation between front and back office of:

The use of mobile phones from within the dealing room for transacting business:

You need to buy USD 5,000,000 against GBP and are quoted the following rates concurrently by two separate banks: 1.6045-50 and 1.6047-52. At which rate do you trade?

A person who appears to be a technician asks for your help in accessing treasury systems as he has forgotten his list of access codes. The Model Code recommends:

Management policy on the use of mobile devices by trading sales and settlement staff should:

Between which departments are clear and structured escalation procedures required for the management of incorrect funding balances?

Using the following rates:

3M (90-day) EUR deposit 0.25%

6M (180-day) EUR deposit 0.50%

What is the rate for a EUR deposit, which runs from 3 to 6 months?

How can material divergences between the value of cash and collateral be managed in a documented sell/buy-back?

A bank expects interest rates to fall with a parallel downward shift in the yield curve. What action should the bank take, if it wants to benefit from this view?

Four banks provide you with quotes in CHF/SEK. Which is the best price for you to buy SEK?

If a 12-month AUD/NZD swap is quoted 53/47, which of the following statements would you consider to be correct?

You are quoted the following market rates:

Spot EUR/USD 1.3010

6M (181-day) EUR 0.30%

6M (181-day) USD 0.50%

What is 6-month EUR/USD?

If making a claim in respect of “use of funds”, payments should be settled within how many days?

Under Basel rules the risk weight for AM-rated claims on corporates in the standardized approach is:

Today, you sell GBP 5,000,000.00 to a customer against JPY for spot value. Tomorrow, the customer defaults. What is your exposure called?

What should a dealer say to express his commitment to putting an additional bid or offer at a current bid or offer price already quoted by his broker?

In the deposit broker market, which one of the following is not a valid reason for the proposed borrower to decline the lenders name?

What is the name of a swap in which the counterparties sell currencies to each other with a concomitant agreement to reverse the exchange of currencies at a fixed date in the future at the same price, and where the interest rates for the two currencies are reflected in the two exchanges but paid separately?

As to general risk management principles, the Model Code mentions that the organizationalstructure should ensure independent risk management and controls. Which one of the following is not among those controls?

Which of the following statements does not explain why banks accept some amount of interest rate risk?

To establish and maintain a short position in deliverable securities, you must:

You deal over the phone with a counterparty. The subsequent confirmation differs from the terms agreed verbally. What is the result?

Your are quoted the following rates:

spot CHF/JPY 60.12-22

3M CHF/JPY 25.5/22.5

At what rate can you buy 3-month outright JPY against CHF?

If a dealer has any intention of assigning an interest rate swap to a third party soon after transacting that swap:

What is one of the responsibilities of the Middle Office according to the Model Code?

How much is a big figure worth per million of base currency it EUR/GBP is 0.6990?

You are quoted the following rates:

Spot JPY/CHF 0.009520-25

6M JPY/CHF 10/7

At what rate can you buy 6-month outright CHF against JPY?

You bought a USD 4,000000 6x9 FRA at 6.75%. The settlement rate is 3-month (90-day) BBA LIBOR, which is fixed at 5.50%. What is the settlement amount at maturity?

If I say that I have “bought and sold” EUR/USD in an FX swap, what have I done?

You have made a price by a Japanese bank in (SD 2,000,000.00 against JPY. They made you

98.95-03 and you took the offer. USD/JPY is now quoted 98.78-81 and you square your position.

What is your profit or loss?

Which of the following statements is false? The repo legal agreement between the two parties concerned should:

Confirmations should be sent out by both counterparties through an efficient and secure means of communication, preferably electronic:

A payer’s 3-month USD LIBOR swap with a remaining term of five years must be reported as:

Deliberately inputting incorrect big figures into an electronic dealing platform is:

A sold JUN 3-month STIR-future should be reported in the gap report as of 22 May:

PDF + Testing Engine

Testing Engine

PDF (Q&A)