Free Practice Questions for the PRMIA PRM Certification 8006 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the PRMIA 8006 exam. To support your certification journey, we have made a selection of our premium 2026 PRM Certification practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

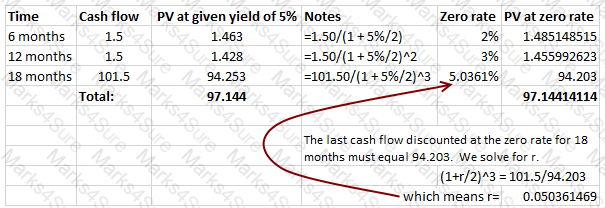

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

What would be the most profitable strategy for an investor who expects interest rates to rise:

Which of the following relationships are true:

I. Delta of Put = Delta of Call - 1

II. Vega of Call = Vega of Put

III. Gamma of Call = Gamma of Put

IV. Theta of Put > Theta of Call

Assume dividends are zero.

The cheapest to deliver bond for a treasury bond futures contract is the one with the :

An investor holds $1m in face each of two bonds. Bond 1 has a price of 90 and a duration of 5 years. Bond 2 has a price of 110 and a duration of 10 years. What is the combined duration of the portfolio in years?

What is the duration of a 10 year zero coupon bond. Assume the bond is callable (ie, the issuer can buy it back) at face value at any time during its existence.

An asset manager is of the view that interest rates are currently high and can only decline over the coming 5 years. He has a choice of investing in the following four instruments, each of which matures in 5 years. Given his perspective, what would be the most suitable investment for the asset manager? Assume a flat yield curve.

What is the standard deviation (in dollars) of a portfolio worth $10,000, of which $4,000 is invested in Stock A, with an expected return of 10% and standard deviation of 20%; and the rest in Stock B, with an expected return of 12% and a standard deviation of 25%. The correlation between the two stocks is 0.6.

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements is true:

I. American options can only be exercised at expiry

II. European options can be exercised at any time up to expiry

III. Bermudan options can be exercised at any time up to expiry except at certain times

IV. A European option can never be worth more than an American option

Which of the following statements are true:

I. An interest rate swap is equivalent to the swap counterparties placing deposits with each other, one carrying a fixed rate of interest and the other a floating rate

II. The parties to a currency swap exchange principals

III. The risky leg in an IRS is the floating rate leg

IV. Swaps do not carry counterparty risks

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

The profit potential from the conversion of convertible bonds into stock is limited by

Which of the following expressions represents the Treynor ratio, where μ is the expected return, σ is the standard deviation of returns, rm is the return of the market portfolio and rf is the risk free rate:

A)

B)

C)

D)

Arrange the following rates in descending order, assuming an upward sloping yield curve:

1. The 10 year zero rate

2. The forward rate from year 9 to 10

3. The yield-to-maturity on a 10 year coupon bearing bond

A portfolio manager desires a position of $10m in physical gold, but chooses to get the exposure using gold futures to conserve cash. The volatility of gold is 6% a month, while that of gold futures is 7% a month. The covariance of gold and gold futures is 0.00378 a month. How many gold contracts should he hold if each contract is worth $100k in gold?

103.11.e1 is the standard deviation of the asset to be hedged, and

103.11.e1 is the standard deviation of the asset to be hedged, and  103.11.e2 is the standard deviation the asset being used to hedge against price movements in x, then the minimum variance hedge ratio is given by the expression

103.11.e2 is the standard deviation the asset being used to hedge against price movements in x, then the minimum variance hedge ratio is given by the expression  103.11.e3 . In this question, correlation = 0.00378/(6%*7%) = 0.9. The minimum variance hedge ratio is given by (6%/7%)*0.9 = 0.77

103.11.e3 . In this question, correlation = 0.00378/(6%*7%) = 0.9. The minimum variance hedge ratio is given by (6%/7%)*0.9 = 0.77 103.11.a3

103.11.a3What is the fair price for a bond paying annual coupons at 5% and maturing in 5 years. Assume par value of $100 and the yield curve is flat at 6%.

An asset manager holds an equity portfolio valued at $25m with a beta of 0.8. She would like to reduce the beta of the portfolio to 0.6 for the next 3 months using index futures. Index futures are curently trading at 1450, and the contract multiple is 250. How should the asset manager trade the index futures to get his desired result? Assume her portfolio is well diversified.

A bank advertises its certificates of deposits as yielding a 5.2% annual effective rate. What is the equivalent continuously compounded rate of return?

Which of the following statements are true:

I. Cash markets tend to be more liquid than derivative markets

II. A higher credit risk is associated with lower liquidity in times of crises

III. A higher bid-ask spread indicates greater liquidity when compared to a lower bid-ask spread

IV. A higher normal market size indicates greater liquidity than a lower market size

It is January and an Australian importer needs to pay USD 1,120,000 at the end of August to a US creditor. If a AUD/USD futures contract is trading on the exchange at a futures price of 0.6750 (ie, 1 AUD = 0.6750 USD), and the contract size is USD 100,000, what would represent an appropriate hedge?

Which of the following is NOT an assumption underlying the Black Scholes Merton option valuation formula:

Which of the following statements are true in respect of a fixed income portfolio:

I. A hedge based on portfolio duration is valid only for small changes in interest rates and needs periodic readjusting

II. A duration based portfolio hedge can be improved by making a convexity adjustment

III. A long position in bonds benefits from the resulting negative convexity

IV. A duration based hedge makes the implicit assumption that only parallel shifts in the yield curve are possible

The price of an interest rate cap is determined by:

I. The period to which the cap relates

II. Volatility of the underlying interest rate

III. The exercise or the strike rate

IV. The risk free rate

Which of the following indicate a long position on the TED (treasury-Eurodollar) spread?

A trader comes in to work and finds the following prices in relation to a stock: $100 spot, $10 for a call expiring in one year with a strike price of $100, and $10 for a put with the same expiry and strike. Interest rates are at 5% per year, and the stock does not pay any dividends. What should the trader do?

If ∆, γ and Θ represent the delta, gamma and theta of any derivative whose value is V; r be the risk free rate; σ be the volatility and S the spot price of the underlying, which of the following equations will hold true? (Note that ∂ is the notation used for partial derivatives)

I. 202.21.q1

II. 202.21.q2

III. 202.21.q3

IV. 202.21.q4

Which of the following is an example of a multifactor model explaining expected asset returns:

I. Arbitrage pricing theory

II. Single index model

III. Capital asset pricing model

What kind of a risk attitude does a utility function with downward sloping curvature indicate?

Calculate the net payment due on a fixed-for-floating interest rate swap where the fixed rate is 5% and the floating rate is LIBOR + 100 basis points. Assume reset dates are every six months, LIBOR at the beginning of the reset period is 4.5% and at the end of the period is 3.5%. Notional is $1m.

Which of the following have a negative gamma:

I. a long call position

II. a short put position

III. a short call position

IV. a long put position

Which of the following statements are true:

I. For a delta neutral portfolio, gamma and theta carry opposite signs

II. The sum of the absolute value of gamma for a call and a put for the same option is 1

III. A large positive gamma is desirable in a delta neutral portfolio

IV. A trader needs at least two separate tradeable options to simultaneously make a portfolio both gamma and vega neutral

Which of the following statements is true in relation to an American style option:

I. Put-call parity applies to American options

II. An American put will never be cheaper than a European put

III. An American put option should never be exercised early for a non-dividend paying stock

IV. An American put option is always at least as valuable as its intrinsic value

Which of the following is true about the early exercise of an American call option:

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements is true:

I. Knock-out options start lifeless and convert to a plain vanilla option when the barrier is hit

II. Barrier options are cheaper than equivalent vanilla options

III. Average price options are more expensive than equivalent vanilla options

IV. Digital options have a high gamma close to the strike price

The annual borrowing rate for investors is 10% per annum. What is the par no-arbitrage futures price for delivery one year hence for a stock currently selling in the spot market at $100 ? Assume the stock pays no dividends.

An asset has a volatility of 10% per year. An investment manager chooses to hedge it with another asset that has a volatility of 9% per year and a correlation of 0.9. Calculate the hedge ratio.

A borrower who fears a rise in interest rates and wishes to hedge against that risk should:

Which of the following will have the effect of increasing the duration of a bond, all else remaining equal:

I. Increase in bond coupon

II. Increase in bond yield

III. Decrease in coupon frequency

IV. Increase in bond maturity

Which of the following statements are true:

I. An yield curve plots zero coupon spot rates for different maturities for bonds with different credit ratings

II. An yield curve represents the term structure of interest rates for similar instruments across a range of maturities

III. The liquidity preference theory explains why the yield curve can be downward sloping

IV. The term structure refers to the relationship between bond yields and bond maturities

If zero rates with continuous compounding for 4 and 5 years are 4% and 5% respectively, what is the forward rate for year 5?

Calculate the basis point value, or PV01, of a bond with a modified duration of 5 and a price of $102.

A bank sells an interest rate swap to its client, with the client agreeing to pay the bank a fixed 4% and receive 3 month LIBOR + 100 basis points, payments due every quarter. After quarter 1, the 3 month LIBOR is 2% pa. Which of the following payments will happen in respect of this swap, assuming the contract notional is $100m, and the rate convention is 30/360.

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following best describes a writer extendible option

Which of the following statements are true?

I. The square-root-of-time rule for scaling volatility over time assumes returns on different days are independent

II. If daily returns are positively correlated, realized volatility will be less than that calculated using the square-root-of time rule

III. If daily returns are negatively correlated, realized volatility will be less than that calculated using the square-root-of-time rule

IV. If stock prices are said to follow a random walk, it means daily returns are independent of each other and have an expected value of zero

A bond pays semi-annual coupons at an annual rate of 10%, and will mature in a year. What is its modified duration? Assume the yield curve is flat for the next 12 months at 5%.

Security A has a beta of 1.2 while security B has a beta of 1.5. If the risk free rate is 3%, and the expected total return from security A is 8%, what is the excess return expected from security B?

What kind of a risk attitude does a utility function with an upward sloping curvature indicate?

A zero coupon bond matures in 5 years and is yielding 5%. What is its modified duration?

Which of the following will have a higher reinvestment risk when compared to a 6% bond issued at par? Assume all bonds have identical yield to maturity.

I. A coupon bearing bond with a coupon rate of 2%

II. An amortizing bond

III. A coupon bearing bond with a coupon rate of 11%

IV. A zero coupon bond

A stock is selling at $90. An investor writes a covered call on the stock with an exercise price of $100 in return for a premium of $3 per share. What would be the maximum gain or loss per share that the investor could make on this position?

In terms of notional values traded, which of the following represents the largest share of total traded futures and options globally?

If the implied volatility for a call option is 30%, the implied volatility for the corresponding put option is:

If interest rates and spot prices stay the same, an increase in the value of a call option will be accompanied by:

The value of which of the following options cannot be less than its intrinsic value

For a portfolio of equally weighted uncorrelated assets, which of the following is FALSE:

The zero rates for 1, 2 and 3 years respectively are 2%, 2.5% and 3% compounded annually. What is the value of an FRA to a bank which will pay 4% on a principal of $10m in year 3?

A fund manager buys a gold futures contract at $1000 per troy ounce, each contract being worth 100 ounces of gold. Initial margin is $5,000 per contract, and the exchange requires a maintenance margin to be maintained at $4,000 per contract. Prices fall the next day to $980. What is the margin call the fund manager faces in respect of daily variation margin ?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

A long call position in an asset-or-nothing option has the same payoff as:

A floating rate note pays daily overnight LIBOR. It matures in exactly one year. What is the duration of the note?

Which of the following statements are true:

I. The swap rate, also called the swap spread, is initially calculated so that the value of the swap at inception is zero.

II. The value of a swap at initiation is different from zero and is equal to the difference between the NPV of the cash flows of the two legs of the swap

III. OTC swaps are standardized and limited to a defined set of standard contracts

IV. Interest rate and commodity swaps are the types of swaps that are most traded

The theta of a delta neutral options position is large and positive. What can we say about the gamma of the position?

It is October. A grower of crops is concerned that January temperatures might be too low and destroy his crop. A heating-degree-days futures contract (HDD futures contract) is available for his city. What would be the best course of action for the grower?

Which of the following assumptions underlie the ' square root of time ' rule used for computing volatility estimates over different time horizons?

I. asset returns are independent and identically distributed (i.i.d.)

II. volatility is constant over time

III. no serial correlation in the forward projection of volatility

IV. negative serial correlations exist in the time series of returns

Which of the following is one of the basic axioms on which the principle of maximum expected utility is based:

How will the Macaulay duration of a 10 year coupon bearing bond change if 10 year zero rates stay the same but the yield curve changes from being flat to upward sloping?

PDF + Testing Engine

Testing Engine

PDF (Q&A)