Free Practice Questions for the PRMIA PRM Certification 8008 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the PRMIA 8008 exam. To support your certification journey, we have made a selection of our premium 2026 PRM Certification practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

Which of the following carry greater counterparty risk: a forward contract on a 10 year note, or a commercial paper carrying a AA credit rating with identical maturity and notional?

Which of the following statements are true:

I. Top down approaches help focus management attention on the frequency and severity of loss events, while bottom up approaches do not.

II. Top down approaches rely upon high level data while bottom up approaches need firm specific risk data to estimate risk.

III. Scenario analysis can help capture both qualitative and quantitative dimensions of operational risk.

Which of the following are measures of liquidity risk

I. Liquidity Coverage Ratio

II. Net Stable Funding Ratio

III. Book Value to Share Price

IV. Earnings Per Share

Which of the following statements are correct?

I. A reliance upon conditional probabilities and a-priori views of probabilities is called the ' frequentist ' view

II. Knightian uncertainty refers to things that might happen but for which probabilities cannot be evaluated

III. Risk mitigation and risk elimination are approaches to reacting to identified risks

IV. Confidence accounting is a reference to the accounting frauds that were seen in the past decade as a reflection of failed governance processes

Which of the following need to be assumed to convert a transition probability matrix for a given time period to the transition probability matrix for another length of time:

I. Time invariance

II. Markov property

III. Normal distribution

IV. Zero skewness

Under the CreditPortfolio View approach to credit risk modeling, which of the following best describes the conditional transition matrix:

The 99% 10-day VaR for a bank is $200mm. The average VaR for the past 60 days is $250mm, and the bank specific regulatory multiplier is 3. What is the bank ' s basic VaR based market risk capital charge?

What would be the consequences of a model of economic risk capital calculation that weighs all loans equally regardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capital requirements

Which of the following are valid approaches to leveraging external loss data for modeling operational risks:

I. Both internal and external losses can be fitted with distributions, and a weighted average approach using these distributions is relied upon for capital calculations.

II. External loss data is used to inform scenario modeling.

III. External loss data is combined with internal loss data points, and distributions fitted to the combined data set.

IV. External loss data is used to replace internal loss data points to create a higher quality data set to fit distributions.

What is the risk horizon period used for credit risk as generally used for economic capital calculations and as required by regulation?

Which of the following is not one of the ' three pillars ' specified in the Basel accord:

A Monte Carlo simulation based VaR can be effectively used in which of the following cases:

Which loss event type is the failure to timely deliver collateral classified as under the Basel II framework?

Which of the following distributions is generally not used for frequency modeling for operational risk

Under the ISDA MA, which of the following terms best describes the netting applied upon the bankruptcy of a party?

If the returns of an asset display a strong tendency for mean reversion, what is the relationship between annualized volatility calculated based on daily versus weekly volatilities (using the square root of time rule)?

When doing stress tests based on historical scenarios, if no appropriate historical scenarios exist for a security, it is most INAPPROPRIATE to:

For the purposes of calculating VaR, an FRA can be modeled as a combination of:

Which of the following is a most complete measure of the liquidity gap facing a firm?

For credit risk calculations, correlation between the asset values of two issuers is often proxied with:

Which of the following statements are true:

I. A transition matrix is the probability of a security migrating from one rating class to another during its lifetime.

II. Marginal default probabilities refer to probabilities of default in a particular period, given survival at the beginning of that period.

III. Marginal default probabilities will always be greater than the corresponding cumulative default probability.

IV. Loss given default is generally greater when recovery rates are low.

A statement in the annual report of a bank states that the 10-day VaR at the 95% level of confidence at the end of the year is $253m. Which of the following is true:

I. The maximum loss that the bank is exposed to over a 10-day period is $253m.

II. There is a 5% probability that the bank ' s losses will not exceed $253m

III. The maximum loss in value that is expected to be equaled or exceeded only 5% of the time is $253m

IV. The bank ' s regulatory capital assets are equal to $253m

Under the standardized approach to calculating operational risk capital under Basel II, negative regulatory capital charges for any of the business units:

A risk analyst analyzing the positions for a proprietary trading desk determines that the combined annual variance of the desk ' s positions is 0.16. The value of the portfolio is $240m. What is the 10-day stand alone VaR in dollars for the desk at a confidence level of 95%? Assume 250 trading days in a year.

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

Which of the following statements are true in relation to Monte Carlo based VaR calculations:

I. Monte Carlo VaR relies upon a full revalution of the portfolio for each simulation

II. Monte Carlo VaR relies upon the delta or delta-gamma approximation for valuation

III. Monte Carlo VaR can capture a wide range of distributional assumptions for asset returns

IV. Monte Carlo VaR is less compute intensive than Historical VaR

The definition of operational risk per Basel II includes which of the following:

I. Risk of loss resulting from inadequate or failed internal processes, people and systems or from external events

II. Legal risk

III. Strategic risk

IV. Reputational risk

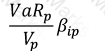

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above

Which of the following statements are true:

I. A high score according to Altman ' s Z-Score methodology indicates a lower default risk

II. A high score according to the Probit or Logit models indicates a higher default risk

III. A high score according to Altman ' s Z-Score methodology indicates a higher default risk

IV. A high score according to the Probit or Logit models indicates a lower default risk

Company A issues bonds with a face value of $100m, sold at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. Company A then defaults, and the recovery rate is expected to be 30%. What is Bank B ' s loss?

The risk that a counterparty fails to deliver its obligation upon settlement while having received the leg owed to it is called:

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

Which of the following are attributes of a robust stress testing programme at a bank?

The sensitivity (delta) of a portfolio to a single point move in the value of the S & P500 is $100. If the current level of the S & P500 is 2000, and has a one day volatility of 1%, what is the value-at-risk for this portfolio at the 99% confidence and a horizon of 10 days? What is this method of calculating VaR called?

Under the CreditPortfolio View model of credit risk, the conditional probability of default will be:

What is the combined VaR of two securities that are perfectly positively correlated.

Which of the following statements is true:

I. Recovery rate assumptions can be easily made fairly accurately given past data available from credit rating agencies.

II. Recovery rate assumptions are difficult to make given the effect of the business cycle, nature of the industry and multiple other factors difficult to model.

III. The standard deviation of observed recovery rates is generally very high, making any estimate likely to differ significantly from realized recovery rates.

IV. Estimation errors for recovery rates are not a concern as they are not directionally biased and will cancel each other out over time.

Which of the following is closest to the description of a ' risk functional ' ?

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving the returns of the S & P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month ' s payments, the bank enters bankruptcy. What is the legal claim that the hedge fund has against the bank in the bankruptcy court?

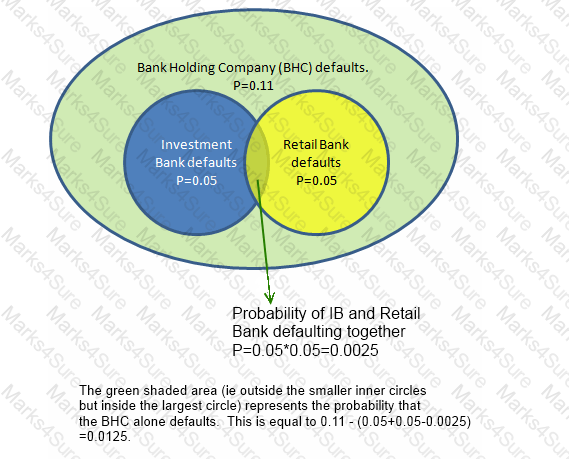

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank ' s defaults are independent of each other, with a probability of default of 0.05 each. The BHC ' s probability of default is 0.11.

What is the probability of default of both the BHC and the investment bank? What is the probability of the BHC ' s default provided both the investment bank and the retail bank survive?

Which of the following statements are true:

I. Shocks to risk factors should be relative rather than absolute if we wish to avoid a change in the sign of the risk factor.

II. Interest rate shocks are generally modeled as absolute shocks.

III. Shocks to volatility are generally modeled as absolute shocks.

IV. Shocks to market spreads are generally modeled as relative shocks.

Which of the following represents a riskier exposure for a bank: A LIBOR based loan, or an Overnight Indexed Swap? Which of the two rates is expected to be higher?

Assume the same counterparty and the same notional.

For a 10 year interest rate swap, what would be the worst time for a counterparty to default (in terms of the maximum likely credit exposure)

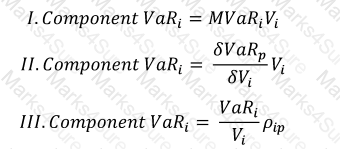

Which of the following formulae correctly describes Component VaR. (p refers to the portfolio, and i is the i-th constituent of the portfolio. MVaR means Marginal VaR, and other symbols have their usual meanings.)

Financial institutions need to take volatility clustering into account:

I. To avoid taking on an undesirable level of risk

II. To know the right level of capital they need to hold

III. To meet regulatory requirements

IV. To account for mean reversion in returns

An assumption of normality when returns data have fat tails leads to:

I. underestimation of VaR at high confidence levels

II. overestimation of VaR at low confidence levels

III. overestimation of VaR at high confidence levels

IV. underestimation of VaR at low confidence levels

Which of the following is not an approach proposed by the Basel II framework to compute operational risk capital?

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel II operational risk categories as:

When estimating the risk of a portfolio of equities using the portfolio ' s beta, which of the following is NOT true:

Which of the following are elements of ' group risk ' :

I. Market risk

II. Intra-group exposures

III. Reputational contagion

IV. Complex group structures

Which of the following statements is a correct description of the phrase present value of a basis point?

Under the contingent claims approach to credit risk, risk increases when:

I. Volatility of the firm ' s assets increases

II. Risk free rate increases

III. Maturity of the debt increases

A derivative contract has a negative current replacement value. Which of the following statements is true about its loan equivalent value for credit risk calculations over a 2-year horizon?

The frequency distribution for operational risk loss events can be modeled by which of the following distributions:

I. The binomial distribution

II. The Poisson distribution

III. The negative binomial distribution

IV. The omega distribution

Calculate the 99% 1-day Value at Risk of a portfolio worth $10m with expected returns of 10% annually and volatility of 20%.

The 10-day VaR of a diversified portfolio is $100m. What is the 20-day VaR of the same portfolio assuming the market shows a trend and the autocorrelation between consecutive periods is 0.2?

For a back office function processing 15,000 transactions a day with an error rate of 10 basis points, what is the annual expected loss frequency (assume 250 days in a year)

According to the implied capital model, operational risk capital is estimated as:

When considering a request for a loan from a retail customer, which of the following factors is relevant for a bank to consider:

According to Basel II ' s definition of operational loss event types, losses due to acts by third parties intended to defraud, misappropriate property or circumvent the law are classified as:

Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

If two bonds with identical credit ratings, coupon and maturity but from different issuers trade at different spreads to treasury rates, which of the following is a possible explanation:

I. The bonds differ in liquidity

II. Events have happened that have changed investor perceptions but these are not yet reflected in the ratings

III. The bonds carry different market risk

IV. The bonds differ in their convexity

Which loss event type is the loss of personally identifiable client information classified as under the Basel II framework?

Under the credit migration approach to assessing portfolio credit risk, which of the following are needed to generate a distribution of future portfolio values?

When compared to a low severity high frequency risk, the operational risk capital requirement for a medium severity medium frequency risk is likely to be:

Stress testing is useful for which of the following purposes:

I. For providing the risk manager with an intuitive check on his risk estimates

II. Providing a means of communicating risk implications using plausible scenarios that can be easily explained to a non-technical audience

III. Guarding against major errors in the form of model risk

IV. Complying with the requirements of Basel II.

Which of the following statements is true?

I. Real Time Gross Systems (RTGS) for large value payments consume less system liquidity than Deferred Net Systems (DNS)

II. The US Fedwire is an example of a Real Time Gross System

III. Current disclosure requirements in relation to liquidity risk as laid down in the Basel framework require banks to disclose how liquidity stress scenarios were formulated

IV. A CFP (Contingency Funding Plan) provides access to Central Bank financing

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

A bullet bond and an amortizing loan are issued at the same time with the same maturity and with the same principal. Which of these would have a greater credit exposure halfway through their life?

Which of the following statements is true?

I. It is sufficient to ensure that a parent entity has sufficient excess liquidity to cover a liquidity shortfall for a subsidiary.

II. If a parent entity has a shortfall of liquidity, it can always rely upon any excess liquidity that its foreign subsidiaries might have.

III. Wholesale funding sources for a bank refer to stable sources of funding provided by the central bank.

IV. Funding diversification refers to diversification of both funding sources and funding tenors.

For the purposes of calculating VaR, an interest rate swap can be modeled as a combination of:

Which of the following are valid techniques used when performing stress testing based on hypothetical test scenarios:

I. Modifying the covariance matrix by changing asset correlations

II. Specifying hypothetical shocks

III. Sensitivity analysis based on changes in selected risk factors

IV. Evaluating systemic liquidity risks

Which of the following statements is true in relation to collateral management?

I. A collateral management system need not consider the failure by counterparties to return collateral when due

II. The extent to which counterparties may have rehypothecated collateral is not a consideration for a collateral management system

III. Cash is an acceptable substitute for any type of collateral required to be posted

IV. Haircuts do not apply to treasury issued instruments posted as collateral

For a US based investor, what is the 10-day value-at risk at the 95% confidence level of a long spot position of EUR 15m, where the volatility of the underlying exchange rate is 16% annually. The current spot rate for EUR is 1.5. (Assume 250 trading days in a year).

Company A issues bonds with a face value of $100m, sold at issuance at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. What is Bank B ' s exposure to the debt issued by Company A?

If the 99% VaR of a portfolio is $82,000, what is the value of a single standard deviation move in the portfolio?

A financial institution is considering shedding a business unit to reduce its economic capital requirements. Which of the following is an appropriate measure of the resulting reduction in capital requirements?

In January, a bank buys a basket of mortgages with a view to securitize them by April. Due to an unexpected lack of investors in the securitization market, it is unable to do so and is left with the exposure to the mortgages on its books. This is an example of:

The Options Theoretic approach to calculating economic capital considers the value of capital as being equivalent to a call option with a strike price equal to:

The CDS rate on a defaultable bond is approximated by which of the following expressions:

According to the Basel II standard, which of the following conditions must be satisfied before a bank can use ' mark-to-model ' for securities in its trading book?

I. Marking-to-market is not possible

II. Market inputs for the model should be sourced in line with market prices

III. The model should have been created by the front office

IV. The model should be subject to periodic review to determine the accuracy of its performance

The probability of default of a security over a 1 year period is 3%. What is the probability that it would have defaulted within 6 months?

What is the 1-day VaR at the 99% confidence interval for a cash flow of $10m due in 6 months time? The risk free interest rate is 5% per annum and its annual volatility is 15%. Assume a 250 day year.

Which of the following objectives are targeted by rating agencies when assigning ratings:

I. Ratings accuracy

II. Ratings stability

III. High accuracy ratio (AR)

IV. Ranked ratings

For a given notional amount, which of the following carries the greatest counterparty exposure (assuming the same counterparty credit rating for each):

Assuming all other factors remain the same, an increase in the volatility of the returns on the assets of a firm causes which of the following outcomes?

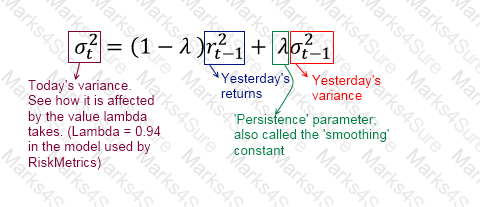

A stock ' s volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter λ = 0.93.

Which of the following is not an event of default covered in the ISDA Master Agreement?

I. failure to pay or deliver

II. credit support default

III. merger without assumption

IV. Bankruptcy

A bank holds $10m of a corporate debt that it has purchased CDS protection against. What is the impact on the short term liquidity of the bank in the event of a default by the corporate on its bonds?

The estimate of historical VaR at 99% confidence based on a set of data with 100 observations will end up being:

PDF + Testing Engine

Testing Engine

PDF (Q&A)