Free Practice Questions for the PRMIA PRM Certification 8010 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the PRMIA 8010 exam. To support your certification journey, we have made a selection of our premium 2026 PRM Certification practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

If P be the transition matrix for 1 year, how can we find the transition matrix for 4 months?

Which of the following are valid approaches to calculating potential future exposure (PFE) for counterparty risk:

I. Add a percentage of the notional to the mark-to-market value

II. Monte Carlo simulation

III. Maximum Likelihood Estimation

IV. Parametric Estimation

For a corporate bond, which of the following statements is true:

I. The credit spread is equal to the default rate times the recovery rate

II. The spread widens when the ratings of the corporate experience an upgrade

III. Both recovery rates and probabilities of default are related to the business cycle and move in opposite directions to each other

IV. Corporate bond spreads are affected by both the risk of default and the liquidity of the particular issue

Which of the following statements is true:

I. When averaging quantiles of two Pareto distributions, the quantiles of the averaged models are equal to the geometric average of the quantiles of the original models based upon the number of data items in each original model.

II. When modeling severity distributions, we can only use distributions which have fewer parameters than the number of datapoints we are modeling from.

III. If an internal loss data based model covers the same risks as a scenario based model, they can can be combined using the weighted average of their parameters.

IV If an internal loss model and a scenario based model address different risks, the models can be combined by taking their sums.

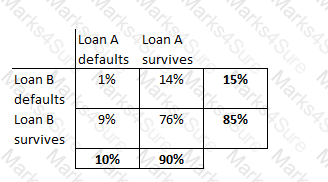

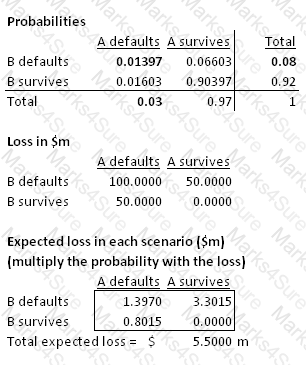

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Under the KMV Moody's approach to calculating expecting default frequencies (EDF), firms' default on obligations is likely when:

The Options Theoretic approach to calculating economic capital considers the value of capital as being equivalent to a call option with a strike price equal to:

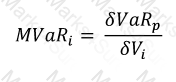

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

Which of the following statements are true:

I. The three pillars under Basel II are market risk, credit risk and operational risk.

II. Basel II is an improvement over Basel I by increasing the risk sensitivity of the minimum capital requirements.

III. Basel II encourages disclosure of capital levels and risks

A bullet bond and an amortizing loan are issued at the same time with the same maturity and with the same principal. Which of these would have a greater credit exposure halfway through their life?

According to the Basel II framework, subordinated term debt that was originally issued 4 years ago with a maturity of 6 years is considered a part of:

Which of the following statements are true?

I. Retail Risk Based Pricing involves using borrower specific data to arrive at both credit adjudication and pricing decisions

II. An integrated 'Risk Information Management Environment' includes two elements - people and processes

III. A Logical Data Model (LDM) lays down the relationships between data elements that an organization stores

IV. Reference Data and Metadata refer to the same thing

Which of the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. A correlation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

Which of the following is true in relation to the application of Extreme Value Theory when applied to operational risk measurement?

I. EVT focuses on extreme losses that are generally not covered by standard distribution assumptions

II. EVT considers the distribution of losses in the tails

III. The Peaks-over-thresholds (POT) and the generalized Pareto distributions are used to model extreme value distributions

IV. EVT is concerned with average losses beyond a given level of confidence

Loss from a lawsuit from an employee due to physical harm caused while at work is categorized per Basel II as:

Which of the following does not affect the credit risk facing a lender institution?

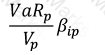

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above

A corporate bond maturing in 1 year yields 8.5% per year, while a similar treasury bond yields 4%. What is the probability of default for the corporate bond assuming the recovery rate is zero?

What ensures that firms are not able to selectively default on some obligations without being considered in default on the others?

If X represents a matrix with ratings transition probabilities for one year, the transition probabilities for 3 years are given by the matrix:

A bank expects the error rate in transaction data entry for a particular business process to be 0.005%. What is the range of expected errors in a day within +/- 2 standard deviations if there are 2,000,000 such transactions each day?

Which of the following are valid methods for selecting an appropriate model from the model space for severity estimation:

I. Cross-validation method

II. Bootstrap method

III. Complexity penalty method

IV. Maximum likelihood estimation method

Company A issues bonds with a face value of $100m, sold at issuance at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. What is Bank B's exposure to the debt issued by Company A?

Which of the following statements is true:

I. Recovery rate assumptions can be easily made fairly accurately given past data available from credit rating agencies.

II. Recovery rate assumptions are difficult to make given the effect of the business cycle, nature of the industry and multiple other factors difficult to model.

III. The standard deviation of observed recovery rates is generally very high, making any estimate likely to differ significantly from realized recovery rates.

IV. Estimation errors for recovery rates are not a concern as they are not directionally biased and will cancel each other out over time.

The 99% 10-day VaR for a bank is $200mm. The average VaR for the past 60 days is $250mm, and the bank specific regulatory multiplier is 3. What is the bank's basic VaR based market risk capital charge?

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving the returns of the S & P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim that the hedge fund has against the bank in the bankruptcy court?

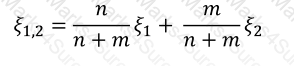

For a hypotherical UoM, the number of losses in two non-overlapping datasets is 24 and 32 respectively. The Pareto tail parameters for the two datasets calculated using the maximum likelihood estimation method are 2 and 3. What is an estimate of the tail parameter of the combined dataset?

If the default hazard rate for a company is 10%, and the spread on its bonds over the risk free rate is 800 bps, what is the expected recovery rate?

When building a operational loss distribution by combining a loss frequency distribution and a loss severity distribution, it is assumed that:

I. The severity of losses is conditional upon the number of loss events

II. The frequency of losses is independent from the severity of the losses

III. Both the frequency and severity of loss events are dependent upon the state of internal controls in the bank

The CDS rate on a defaultable bond is approximated by which of the following expressions:

Which of the following credit risk models focuses on default alone and ignores credit migration when assessing credit risk?

What would be the correct order of steps to addressing data quality problems in an organization?

An operational loss severity distribution is estimated using 4 data points from a scenario. The management institutes additional controls to reduce the severity of the loss if the risk is realized, and as a result the estimated losses from a 1-in-10-year losses are halved. The 1-in-100 loss estimate however remains the same. What would be the impact on the 99.9th percentile capital required for this risk as a result of the improvement in controls?

Under the actuarial (or CreditRisk+) based modeling of defaults, what is the probability of 4 defaults in a retail portfolio where the number of expected defaults is 2?

Which of the following statements is true:

I. Basel II requires banks to conduct stress testing in respect of their credit exposures in addition to stress testing for market risk exposures

II. Basel II requires pooled probabilities of default (and not individual PDs for each exposure) to be used for credit risk capital calculations

The sum of the stand alone economic capital of all the business units of a bank is:

For a 10 year interest rate swap, what would be the worst time for a counterparty to default (in terms of the maximum likely credit exposure)

Under the contingent claims approach to credit risk, risk increases when:

I. Volatility of the firm's assets increases

II. Risk free rate increases

III. Maturity of the debt increases

Which of the following credit risk models includes a consideration of macro economic variables such as unemployment, balance of payments etc to assess credit risk?

For a group of assets known to be positively correlated, what is the impact on economic capital calculations if we assume the assets to be independent (or uncorrelated)?

Under the credit migration approach to assessing portfolio credit risk, which of the following are needed to generate a distribution of future portfolio values?

When modeling operational risk using separate distributions for loss frequency and loss severity, which of the following is true?

A key problem with return on equity as a measure of comparative performance is:

Which of the following statements are true:

I. Top down approaches help focus management attention on the frequency and severity of loss events, while bottom up approaches do not.

II. Top down approaches rely upon high level data while bottom up approaches need firm specific risk data to estimate risk.

III. Scenario analysis can help capture both qualitative and quantitative dimensions of operational risk.

Which loss event type is the failure to timely deliver collateral classified as under the Basel II framework?

Which of the following statements are correct:

I. A training set is a set of data used to create a model, while a control set is a set of data is used to prove that the model actually works

II. Cleansing, aggregating or ensuring data integrity is a task for the IT department, and is not a risk manager's responsibility

III. Lack of information on the quality of underlying securities and assets was a major cause of the collapse in the CDO markets during the credit crisis that started in 2007

IV. The problem of lack of historical data can be addressed reasonably satisfactorily by using analytical approaches

A risk analyst peforming PCA wishes to explain 80% of the variance. The first orthogonal factor has a volatility of 100, and the second 40, and the third 30. Assume there are no other factors. Which of the factors will be included in the final analysis?

Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

Under the CreditPortfolio View approach to credit risk modeling, which of the following best describes the conditional transition matrix:

Which of the following event types is hacking damage classified under Basel II operational risk classifications?

Which of the following statements are true:

I. Capital adequacy implies the ability of a firm to remain a going concern

II. Regulatory capital and economic capital are identical as they target the same objectives

III. The role of economic capital is to provide a buffer against expected losses

IV. Conservative estimates of economic capital are based upon a confidence level of 100%

Under the internal ratings based approach for risk weighted assets, for which of the following parameters must each institution make internal estimates (as opposed to relying upon values determined by a national supervisor):

When compared to a high severity low frequency risk, the operational risk capital requirement for a low severity high frequency risk is likely to be:

Which of the following is not a permitted approach under Basel II for calculating operational risk capital

Which of the following statements is true

I. If no loss data is available, good quality scenarios can be used to model operational risk

II. Scenario data can be mixed with observed loss data for modeling severity and frequency estimates

III. Severity estimates should not be created by fitting models to scenario generated loss data points alone

IV. Scenario assessments should only be used as modifiers to ILD or ELD severity models.

Under the KMV Moody's approach to credit risk measurement, how is the distance to default converted to expected default frequencies?

If F be the face value of a firm's debt, V the value of its assets and E the market value of equity, then according to the option pricing approach a default on debt occurs when:

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the default correlation is 25%, what is the one year expected loss on this portfolio?

Which of the following statements are true:

I. Credit risk and counterparty risk are synonymous

II. Counterparty risk is the contingent risk from a counterparty's default in derivative transactions

III. Counterparty risk is the risk of a loan default or the risk from moneys lent directly

IV. The exposure at default is difficult to estimate for credit risk as it depends upon market movements

PDF + Testing Engine

Testing Engine

PDF (Q&A)