Free Practice Questions for the PRMIA PRM Certification 8011 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the PRMIA 8011 exam. To support your certification journey, we have made a selection of our premium 2026 PRM Certification practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

Which of the following are true:

I. Delta hedges need to be rebalanced frequently as deltas fluctuate with fluctuating prices.

II. Portfolio managers are right to focus on primary risks over secondary risks.

III. Increasing the hedge rebalance frequency reduces residual risks but increases transaction costs.

IV. Vega risk can be hedged using options.

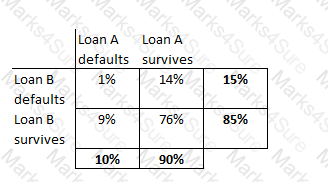

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

A white rectangular grid with black text

Description automatically generated

A white rectangular grid with black text

Description automatically generatedWhich of the following are considered asset based credit enhancements?

I. Collateral

II. Credit default swaps

III. Close out netting arrangements

IV. Cash reserves

A bank holds a portfolio of corporate bonds. Corporate bond spreads widen, resulting in a loss of value for the portfolio. This loss arises due to:

Which of the following credit risk models relies upon the analysis of credit rating migrations to assess credit risk?

The daily VaR of an investor's commodity position is $10m. The annual VaR, assuming daily returns are independent, is ~$158m (using the square root of time rule). Which of the following statements are correct?

I. If daily returns are not independent and show mean-reversion, the actual annual VaR will be higher than $158m.

II. If daily returns are not independent and show mean-reversion, the actual annual VaR will be lower than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be higher than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be lower than $158m.

Which of the following statements is true:

I. If the sum of its parameters is less than one, GARCH is a mean reverting model of volatility, while EWMA is never mean reverting

II. Standardized returns under both EWMA and GARCH show less non-normality than non standardized returns

III. Steady state variance under GARCH is affected only by the persistence coefficient

IV. Good risk measures are always sub-additive

Which of the following is true in relation to Principal Component Analysis (PCA)?

I. An n x n positive definite square matrix will have n-1 eigenvectors

II. The eigenvalues for a correlation matrix can be derived from the corresponding values for the covariance matrix

III. Principal components are uncorrelated to each other

IV. PCA is useful as it allows 100% of the variation in a complex system to be explained by the first three principal components

Which of the following statements are true in relation to Monte Carlo based VaR calculations:

I. Monte Carlo VaR relies upon a full revalution of the portfolio for each simulation

II. Monte Carlo VaR relies upon the delta or delta-gamma approximation for valuation

III. Monte Carlo VaR can capture a wide range of distributional assumptions for asset returns

IV. Monte Carlo VaR is less compute intensive than Historical VaR

Which of the following statements is true:

I. Expected credit losses are charged to the unit's P & L while unexpected losses hit risk capital reserves.

II. Credit portfolio loss distributions are symmetrical

III. For a bank holding $10m in face of a defaulted debt that it acquired for $2m, the bank's legal claim in the bankruptcy court will be $10m.

IV. The legal claim in bankruptcy court for an over the counter derivatives contract will be the notional value of the contract.

A bank extends a loan of $1m to a home buyer to buy a house currently worth $1.5m, with the house serving as the collateral. The volatility of returns (assumed normally distributed) on house prices in that neighborhood is assessed at 10% annually. The expected probability of default of the home buyer is 5%.

What is the probability that the bank will recover less than the principal advanced on this loan; assuming the probability of the home buyer's default is independent of the value of the house?

Which of the following are measures of liquidity risk

I. Liquidity Coverage Ratio

II. Net Stable Funding Ratio

III. Book Value to Share Price

IV. Earnings Per Share

Which of the following credit risk models includes a consideration of macro economic variables such as unemployment, balance of payments etc to assess credit risk?

Which of the following statements is true:

I. When averaging quantiles of two Pareto distributions, the quantiles of the averaged models are equal to the geometric average of the quantiles of the original models based upon the number of data items in each original model.

II. When modeling severity distributions, we can only use distributions which have fewer parameters than the number of datapoints we are modeling from.

III. If an internal loss data based model covers the same risks as a scenario based model, they can can be combined using the weighted average of their parameters.

IV If an internal loss model and a scenario based model address different risks, the models can be combined by taking their sums.

A black line with letters and numbers

Description automatically generated

A black line with letters and numbers

Description automatically generatedWhich of the following statements are correct:

I. A training set is a set of data used to create a model, while a control set is a set of data is used to prove that the model actually works

II. Cleansing, aggregating or ensuring data integrity is a task for the IT department, and is not a risk manager's responsibility

III. Lack of information on the quality of underlying securities and assets was a major cause of the collapse in the CDO markets during the credit crisis that started in 2007

IV. The problem of lack of historical data can be addressed reasonably satisfactorily by using analytical approaches

Which of the following statements are true:

I. Top down approaches help focus management attention on the frequency and severity of loss events, while bottom up approaches do not.

II. Top down approaches rely upon high level data while bottom up approaches need firm specific risk data to estimate risk.

III. Scenario analysis can help capture both qualitative and quantitative dimensions of operational risk.

Which of the following statements is NOT true in relation to the recent financial crisis of 2007-08?

Which of the following assumptions underlie the 'square root of time' rule used for computing VaR estimates over different time horizons?

I. the portfolio is static from day to day

II. asset returns are independent and identically distributed (i.i.d.)

III. volatility is constant over time

IV. no serial correlation in the forward projection of volatility

V. negative serial correlations exist in the time series of returns

VI. returns data display volatility clustering

The 99% 10-day VaR for a bank is $200mm. The average VaR for the past 60 days is $250mm, and the bank specific regulatory multiplier is 3. What is the bank's basic VaR based market risk capital charge?

If F be the face value of a firm's debt, V the value of its assets and E the market value of equity, then according to the option pricing approach a default on debt occurs when:

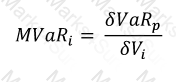

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

A mathematical equation with numbers and symbols

Description automatically generated

A mathematical equation with numbers and symbols

Description automatically generatedWhich of the following is a most complete measure of the liquidity gap facing a firm?

The estimate of historical VaR at 99% confidence based on a set of data with 100 observations will end up being:

Which of the following is true in relation to the application of Extreme Value Theory when applied to operational risk measurement?

I. EVT focuses on extreme losses that are generally not covered by standard distribution assumptions

II. EVT considers the distribution of losses in the tails

III. The Peaks-over-thresholds (POT) and the generalized Pareto distributions are used to model extreme value distributions

IV. EVT is concerned with average losses beyond a given level of confidence

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

Which of the following situations are not suitable for applying parametric VaR:

I. Where the portfolio's valuation is linearly dependent upon risk factors

II. Where the portfolio consists of non-linear products such as options and large moves are involved

III. Where the returns of risk factors are known to be not normally distributed

For a given mean, which distribution would you prefer for frequency modeling where operational risk events are considered dependent, or in other words are seen as clustering together (as opposed to being independent)?

Who has the ultimate responsibility for the overall stress testing programme of an institution?

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

When building a operational loss distribution by combining a loss frequency distribution and a loss severity distribution, it is assumed that:

I. The severity of losses is conditional upon the number of loss events

II. The frequency of losses is independent from the severity of the losses

III. Both the frequency and severity of loss events are dependent upon the state of internal controls in the bank

The key difference between 'top down models' and 'bottom up models' for operational risk assessment is:

Which of the following statements are true:

I. The sum of unexpected losses for individual loans in a portfolio is equal to the total unexpected loss for the portfolio.

II. The sum of unexpected losses for individual loans in a portfolio is less than the total unexpected loss for the portfolio.

III. The sum of unexpected losses for individual loans in a portfolio is greater than the total unexpected loss for the portfolio.

IV. The unexpected loss for the portfolio is driven by the unexpected losses of the individual loans in the portfolio and the default correlation between these loans.

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that exactly 1 of the three bonds will default.

Which of the following objectives are targeted by rating agencies when assigning ratings:

I. Ratings accuracy

II. Ratings stability

III. High accuracy ratio (AR)

IV. Ranked ratings

In setting confidence levels for VaR estimates for internal limit setting, it is generally desirable:

Which of the following are ordered correctly in the order of debt seniority in a bankruptcy situation?

I. Equity, Subordinate debt, Senior debt

II. Senior debt, Preferred stock, Equity

III. Secured debt, Accounts payable, Preferred stock

IV. Secured debt, DIP financing, Equity

A bank expects the error rate in transaction data entry for a particular business process to be 0.005%. What is the range of expected errors in a day within +/- 2 standard deviations if there are 2,000,000 such transactions each day?

Which of the following is not a possible early warning indicator in relation to the health of a counterparty?

Ex-ante VaR estimates may differ from realized P & L due to:

I. the effect of intra day trading

II. timing differences in the accounting systems

III. incorrect estimation of VaR parameters

IV. security returns exhibiting mean reversion

The principle underlying the contingent claims approach to measuring credit risk equates the cost of eliminating credit risk for a firm to be equal to:

Which of the following statements are true:

I. Heavy tailed parametric distributions are a good choice for severity modeling in operational risk.

II. Heavy tailed body-tail distributions are a good choice for severity modeling in operational risk.

III. Log-likelihood is a means to estimate parameters for a distribution.

IV. Body-tail distributions allow modeling small losses differently from large ones.

If the marginal probabilities of default for a corporate bond for years 1, 2 and 3 are 2%, 3% and 4% respectively, what is the cumulative probability of default at the end of year 3?

Calculate the 99% 1-day Value at Risk of a portfolio worth $10m with expected returns of 10% annually and volatility of 20%.

Which of the following describes rating transition matrices published by credit rating firms:

Which of the following statements is true?

I. It is sufficient to ensure that a parent entity has sufficient excess liquidity to cover a liquidity shortfall for a subsidiary.

II. If a parent entity has a shortfall of liquidity, it can always rely upon any excess liquidity that its foreign subsidiaries might have.

III. Wholesale funding sources for a bank refer to stable sources of funding provided by the central bank.

IV. Funding diversification refers to diversification of both funding sources and funding tenors.

Which loss event type is the loss of personally identifiable client information classified as under the Basel II framework?

Which of the following does not affect the credit risk facing a lender institution?

Which of the following are likely to be useful to a risk manager analyzing liquidity risk for an international bank?

I. Information on liquidity mismatches

II. Funding concentration

III. Lending concentration

IV. A report on illiquid assets

Which of the following is not a permitted approach under Basel II for calculating operational risk capital

If the annual variance for a portfolio is 0.0256, what is the daily volatility assuming there are 250 days in a year.

What would be the consequences of a model of economic risk capital calculation that weighs all loans equally regardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capital requirements

A long position in a credit sensitive bond can be synthetically replicated using:

A zero coupon corporate bond maturing in an year has a probability of default of 5% and yields 12%. The recovery rate is zero. What is the risk free rate?

When estimating the risk of a portfolio of equities using the portfolio's beta, which of the following is NOT true:

Which of the following steps are required for computing the aggregate distribution for a UoM for operational risk once loss frequency and severity curves have been estimated:

I. Simulate number of losses based on the frequency distribution

II. Simulate the dollar value of the losses from the severity distribution

III. Simulate random number from the copula used to model dependence between the UoMs

IV. Compute dependent losses from aggregate distribution curves

The unexpected loss for a credit portfolio at a given VaR estimate is defined as:

A statement in the annual report of a bank states that the 10-day VaR at the 95% level of confidence at the end of the year is $253m. Which of the following is true:

I. The maximum loss that the bank is exposed to over a 10-day period is $253m.

II. There is a 5% probability that the bank's losses will not exceed $253m

III. The maximum loss in value that is expected to be equaled or exceeded only 5% of the time is $253m

IV. The bank's regulatory capital assets are equal to $253m

According to the implied capital model, operational risk capital is estimated as:

For a back office function processing 15,000 transactions a day with an error rate of 10 basis points, what is the annual expected loss frequency (assume 250 days in a year)

When compared to a low severity high frequency risk, the operational risk capital requirement for a medium severity medium frequency risk is likely to be:

Under the KMV Moody's approach to credit risk measurement, how is the distance to default converted to expected default frequencies?

If the full notional value of a debt portfolio is $100m, its expected value in a year is $85m, and the worst value of the portfolio in one year's time at 99% confidence level is $60m, then what is the credit VaR?

Which of the following statements is true?

I. Real Time Gross Systems (RTGS) for large value payments consume less system liquidity than Deferred Net Systems (DNS)

II. The US Fedwire is an example of a Real Time Gross System

III. Current disclosure requirements in relation to liquidity risk as laid down in the Basel framework require banks to disclose how liquidity stress scenarios were formulated

IV. A CFP (Contingency Funding Plan) provides access to Central Bank financing

Which of the following techniques is used to generate multivariate normal random numbers that are correlated?

Which of the following statements is true:

I. Recovery rate assumptions can be easily made fairly accurately given past data available from credit rating agencies.

II. Recovery rate assumptions are difficult to make given the effect of the business cycle, nature of the industry and multiple other factors difficult to model.

III. The standard deviation of observed recovery rates is generally very high, making any estimate likely to differ significantly from realized recovery rates.

IV. Estimation errors for recovery rates are not a concern as they are not directionally biased and will cancel each other out over time.

For credit risk calculations, correlation between the asset values of two issuers is often proxied with:

A bullet bond and an amortizing loan are issued at the same time with the same maturity and with the same principal. Which of these would have a greater credit exposure halfway through their life?

Which of the following is the most accurate description of EPE (Expected Positive Exposure):

Under the KMV Moody's approach to calculating expecting default frequencies (EDF), firms' default on obligations is likely when:

Which loss event type is the failure to timely deliver collateral classified as under the Basel II framework?

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

Which of the following statements is the most appropriate description of feedback effects:

Which of the following is the most important problem to solve for fitting a severity distribution for operational risk capital:

If an institution has $1000 in assets, and $800 in liabilities, what is the economic capital required to avoid insolvency at a 99% level of confidence? The VaR in respect of the assets at 99% confidence over a one year period is $100.

If the default hazard rate for a company is 10%, and the spread on its bonds over the risk free rate is 800 bps, what is the expected recovery rate?

For the purposes of calculating VaR, an interest rate swap can be modeled as a combination of:

The definition of operational risk per Basel II includes which of the following:

I. Risk of loss resulting from inadequate or failed internal processes, people and systems or from external events

II. Legal risk

III. Strategic risk

IV. Reputational risk

If A and B be two uncorrelated securities, VaR(A) and VaR(B) be their values-at-risk, then which of the following is true for a portfolio that includes A and B in any proportion. Assume the prices of A and B are log-normally distributed.

Pick underlying risk factors for a position in an equity index option:

I. Spot value for the index

II. Risk free interest rate

III. Volatility of the underlying

IV. Strike price for the option

PDF + Testing Engine

Testing Engine

PDF (Q&A)