Free Practice Questions for the PRMIA PRM Certification 8013 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the PRMIA 8013 exam. To support your certification journey, we have made a selection of our premium 2026 PRM Certification practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

Which of the following are considered Credit Events under ISDA definitions?

I. Bankruptcy

II. Obligation Acceleration

III. Obligation Default

IV. Restructuring

In the context of futures contracts traded on an exchange, the term 'open interest' refers to:

Which of the following statements are true:

I. The swap rate, also called the swap spread, is initially calculated so that the value of the swap at inception is zero.

II. The value of a swap at initiation is different from zero and is equal to the difference between the NPV of the cash flows of the two legs of the swap

III. OTC swaps are standardized and limited to a defined set of standard contracts

IV. Interest rate and commodity swaps are the types of swaps that are most traded

A borrower who fears a rise in interest rates and wishes to hedge against that risk should:

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

The profit potential from the conversion of convertible bonds into stock is limited by

What kind of a risk attitude does a utility function with downward sloping curvature indicate?

An investor holds $1m in a 10 year bond that has a basis point value (or PV01) of 5 cents. She seeks to hedge it using a 30 year bond that has a BPV of 8 cents. How much of the 30 year bond should she buy or sell to hedge against parallel shifts in the yield curve?

Using a single step binomial model, calculate the delta of a call option where future stock prices can take the values $102 and $98, and the call option payoff is $1 if the price goes up, and zero if the price goes down. Ignore interest.

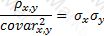

The effectiveness of a hedge is determined by which of the following expressions, where ρ x,y is the correlation between the asset being hedged and the hedge position:

A)

B)

C)

D)

The rate of dividend on a stock goes up. What is the effect on the price of a call option on this stock?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

What is the current conversion premium for a convertible bond where $100 in market value of the bond is convertible into two shares and the current share price is $50?

Which of the following are valid credit enhancements used for credit derivatives:

I. Overcollateralization

II. Excess spread

III. Cash reserves

IV. Margin requirements

Which of the following is NOT true about a fixed rate bond:

I. The higher the coupon, the lower the duration

II. The higher the coupon, the lower the convexity

III. If the bond is callable, it has negative modified duration

IV. If the bond is callable, the bond has negative convexity

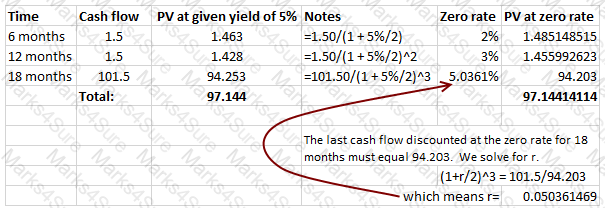

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

It is January. Which of the following is an appropriate hedging strategy for a corn farmer expecting a harvest in June?

If the current stock price is $100, the risk-free rate of interest is 10% per year, and the value of a put option expiring in 1 year on this stock at a strike price of $110 is $5. What is the value of the call option with the same strike?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements relating to convertible debt are true:

I. A hard call protection means the bond cannot be called by the issuer till the share price reaches a threshold

II. It is advantageous for the issuer to call its convertible securities when the share price exceeds the conversion price

III. When the issuer's share prices is very high, the convertible bond trades at a discount to the value of the shares it is convertible into

IV. Convertible bonds generally have to carry a higher coupon than on equivalent non-convertible securities to make them attractive to investors

When considering an appropriate mix of debt and equity, Chief Financial Officers generally consider:

I. Tax advantage of debt

II. Financial distress costs

III. Agency costs of equity

IV. Retaining financial flexibility

Determine the price of a 3 year bond paying a 5% coupon. The 1,2 and 3 year spot rates are 5%, 6% and 7% respectively. Assume a face value of $100.

Security A has a beta of 1.2 while security B has a beta of 1.5. If the risk free rate is 3%, and the expected total return from security A is 8%, what is the excess return expected from security B?

Which of the following statements are true:

I. For a delta neutral portfolio, gamma and theta carry opposite signs

II. The sum of the absolute value of gamma for a call and a put for the same option is 1

III. A large positive gamma is desirable in a delta neutral portfolio

IV. A trader needs at least two separate tradeable options to simultaneously make a portfolio both gamma and vega neutral

Calculate the number of S & P futures contracts to sell to hedge the market exposure of an equity portfolio value at $1m and with a β of 1.5. The S & P is currently at 1000 and the contract multiplier is 250.

Calculate the settlement amount for a buyer of a 3 x 6 FRA with a notional of $1m and contract rate of 5%. Assume settlement rate is 6%.

Assuming all other factors remain the same, an increase in the volatility of the returns on the assets of a firm causes which of the following outcomes?

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. What is the bond's price?

Which of the following statements are true in respect of a fixed income portfolio:

I. A hedge based on portfolio duration is valid only for small changes in interest rates and needs periodic readjusting

II. A duration based portfolio hedge can be improved by making a convexity adjustment

III. A long position in bonds benefits from the resulting negative convexity

IV. A duration based hedge makes the implicit assumption that only parallel shifts in the yield curve are possible

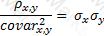

The relationship between covariance and correlation for two assets x and y is expressed by which of the following equations (where covar x,y is the covariance between x and y , σ x and σ y are the respective standard deviations and ρ x,y is the correlation between x and y ):

A)

B)

C)

D)

None of the above

Which of the following statements are true:

I. Rebalancing frequency is a consideration for a risk manager when assessing the adequacy of delta hedging procedures on an options portfolio

II. Stock options granted to employees that are exercisable 5 years in the future will lead to a decline in the share price 5 years hence only if the options are exercised.

III. In a delta neutral portfolio, theta is often used as a proxy for gamma by traders.

IV. Vega is highest when the option price is close to the strike price

If ∆, γ and Θ represent the delta, gamma and theta of any derivative whose value is V; r be the risk free rate; σ be the volatility and S the spot price of the underlying, which of the following equations will hold true? (Note that ∂ is the notation used for partial derivatives)

I. 202.21.q1

II. 202.21.q2

III. 202.21.q3

IV. 202.21.q4

A stock is selling at $90. An investor writes a covered call on the stock with an exercise price of $100 in return for a premium of $3 per share. What would be the maximum gain or loss per share that the investor could make on this position?

When hedging one fixed income security with another, the hedge ratio is determined by:

Which of the following statements are true:

I. All investors regardless of their expectations face the same efficient frontier which is always the market portfolio

II. Investors will have different efficient frontiers based upon their views of expected risks, returns and correlations

III. Investors risk appetite will determine their choice of the combination of risk-free and risky assets to hold

IV. If all investors have identical views on expected returns, standard deviation and correlations, they will hold risky assets in identical proportions

Basis risk between spot and futures prices for stock indices is caused by changes in:

I. The risk free rate, or the funding cost for the futures

II. Expected dividend yield

III. Volatility of the underlying stock index

Which of the following statements are true?

I. Macaulay duration of a coupon bearing bond is unaffected by changes in the curvature of the yield curve.

II. The numerical value for modified duration will be different for bonds with identical nominal coupons and maturity but different compounding frequencies.

III. When rates are expressed as continuously compounded, modified duration and Macaulay duration are the same.

IV. Convexity is higher for a bond with a lower coupon when compared to a similar bond with a higher coupon.

Which of the following is NOT an assumption underlying the Black Scholes Merton option valuation formula:

Repos are used for:

I. Short term borrowings

II. Managing credit risk exposures

III. Money market operations by central banks

IV. Facilitating short positions

Which of the following is NOT an assumption underlying the Black Scholes Merton option valuation formula:

If zero rates with continuous compounding for 4 and 5 years are 4% and 5% respectively, what is the forward rate for year 5?

What is the yield to maturity for a 5% annual coupon bond trading at par? The bond matures in 10 years.

Security A and B both have expected returns of 10%, but the standard deviation of Security A is 10% while that of security B is 20%. Borrowings are not permitted. A portfolio manager who wishes to maximize his probability of earning a 25% return during the year should invest in:

An investor in mortgage backed securities can hedge his/her prepayment risk using which of the following?

I. Long swaption

II. Short cap

III. Short callable bonds

IV. Long fixed/floating swap

A borrower pays a floating rate on a loan and wishes to convert it to a position where a fixed rate is paid. Which of the following can be used to accomplish this objective?

I. A short position in a fixed rate bond and a long position in an FRN

II. An long position in an interest rate collar and long an FRN

III. A short position in a fixed rate bond and a short position in an FRN

IV. An interest rate swap where the investor pays the fixed rate

The securities market line (SML) based upon the CAPM expresses the relationship between

An asset manager is of the view that interest rates are currently high and can only decline over the coming 5 years. He has a choice of investing in the following four instruments, each of which matures in 5 years. Given his perspective, what would be the most suitable investment for the asset manager? Assume a flat yield curve.

Which of the following statements is true:

I. The maximum value of the delta of a call option can be infinity

II. The value of theta for a deep out of the money call approaches zero

III. The vega for a put option is negative

IV. For a at the money cash-or-nothing digital option, gamma approaches zero

A zero coupon bond matures in 5 years and is yielding 5%. What is its modified duration?

An asset has a volatility of 10% per year. An investment manager chooses to hedge it with another asset that has a volatility of 9% per year and a correlation of 0.9. Calculate the hedge ratio.

If the 3 month interest rate is 5%, and the 6 month interest rate is 6%, what would be the contract rate applicable to a 3 x 6 FRA?

A 'consol' is a perpetual bond issued by the UK government. Its running yield is 5%. What is its duration?

An investor expects stock prices to move either sharply up or down. His preferred strategy should be to:

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the 2 year swap rate is 5%, and the yield curve is also flat at 5%

What is the standard deviation (in dollars) of a portfolio worth $10,000, of which $4,000 is invested in Stock A, with an expected return of 10% and standard deviation of 20%; and the rest in Stock B, with an expected return of 12% and a standard deviation of 25%. The correlation between the two stocks is 0.6.

For a stock that does not pay dividends, which of the following represents the delta of a futures contract?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements are true for a contingent premium option:

I. They are also called 'pay-later' options

II. Premiums are due only if the option expires in the money

III. They are a combination of a vanilla option and an appropriate number of cash-or-nothing options

IV. They are preferred because the premiums are always less than those on equivalent vanilla options

Using covered interest parity, calculate the 3 month CAD/USD forward rate if the spot CAD/USD rate is 1.1239 and the three month interest rates on CAD and USD are 0.75% and 0.4% annually respectively.

Calculate the basis point value, or PV01, of a bond with a modified duration of 5 and a price of $102.

If the implied volatility for a call option is 30%, the implied volatility for the corresponding put option is:

If the implied volatility is known for a call option, what can be said about the implied volatility for a put option with the same strike and maturity?

https://riskprep.com/images/stories/questions/102.07.a.png is the coefficient of risk aversion at x. Its inverse, ie

https://riskprep.com/images/stories/questions/102.07.a.png is the coefficient of risk aversion at x. Its inverse, ie  https://riskprep.com/images/stories/questions/102.07.b.png , is called the coefficient of risk tolerance.

https://riskprep.com/images/stories/questions/102.07.b.png , is called the coefficient of risk tolerance.Which of the following expressions represents Jensen's alpha, where μ is the expected return, σ is the standard deviation of returns, rm is the return of the market portfolio and rf is the risk free rate:

Options:

https://www.riskprep.com/images/stories/questions/102.12.b.png

https://www.riskprep.com/images/stories/questions/102.12.b.png

B)

<a href="https://www.riskprep.com/images/stories/questions/102.12.d.png">https://www.riskprep.com/images/storie

<a href="https://www.riskprep.com/images/stories/questions/102.12.d.png">https://www.riskprep.com/images/storie

Option A

Option B

Option C

Option D

Which of the following have a negative gamma:

I. a long call position

II. a short put position

III. a short call position

IV. a long put position

The annual borrowing rate for investors is 10% per annum. What is the par no-arbitrage futures price for delivery one year hence for a stock currently selling in the spot market at $100 ? Assume the stock pays no dividends.

A pension fund has $100m in liabilities due in the future with an average modified duration of 20 years. The fund also holds a fixed income portfolio worth $125m with an average duration of 15 years. Which of the following approaches would be best suited for the pension fund to cover its interest rate risk?

For a portfolio of equally weighted uncorrelated assets, which of the following is FALSE:

PDF + Testing Engine

Testing Engine

PDF (Q&A)