Free Practice Questions for the CIMA Operational P1 Exam (2026 Updated)

At Marks4sure, we are dedicated to providing IT professionals with the most accurate and reliable preparation materials for the CIMA P1 exam. To support your certification journey, we have made a selection of our premium 2026 CIMA Operational practice questions and answers available completely free. You can take this practice test as many times as you need. Every question includes a detailed, expertly verified explanation to ensure you fully grasp the core security concepts before test day.

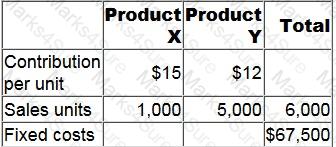

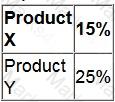

A company sells two products, X and Y, which are always sold in the same ratio.

No inventories are held.

The following budgeted data relate to month 10:

What is the budgeted margin of safety in month 10?

Which one of the following would NOT be included in a decision to close a division of an organization?

A company makes two products, product X with a contribution per unit of $10 and product Y with a contribution per unit of $4.

These products are sold in the mix 3:2 by volume and fixed costs are $38,000 per period.

The breakeven point for product Y, based on the expected sales mix is:

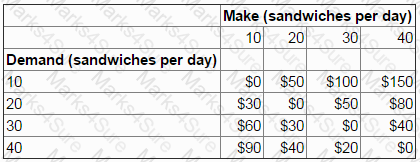

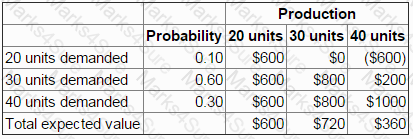

The manager of a recently opened cafe is deciding how many sandwiches to make each day.

The sandwiches are made in the morning before the cafe opens.

If demand exceeds the number of sandwiches made in the morning no extra sandwiches can be made during the day. Any unsold sandwiches are thrown away at the end of each day.

Daily demand is uncertain but is predicted to be 10, 20, 30 or 40 sandwiches.

The following regret matrix has been prepared:

If the minimax regret criterion is used to make the decision, the manager will choose to make:

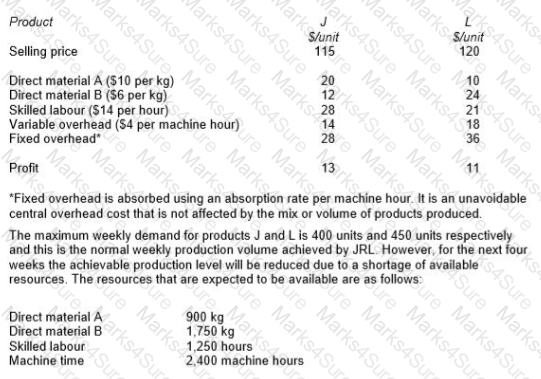

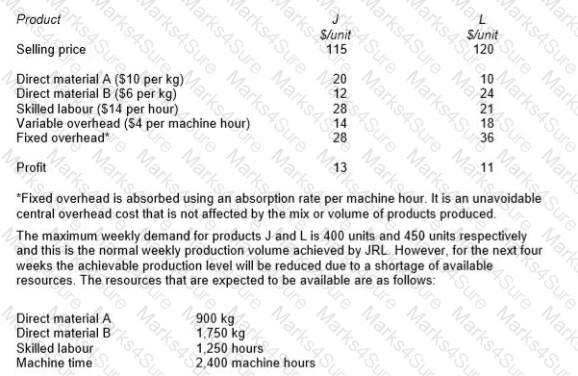

JRL manufactures two products from different combinations of the same resources. Unit selling prices and unit cost details for each product are as follows:

* Refer to your answer in the previous question.

The optimal solution to the previous question shows that the shadow prices of skilled labour and direct material A are as follows:

Skilled labour $ Nil Direct Material A $11.70

Explain the relevance of these values to the management of JRL.

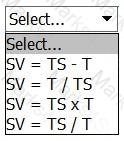

Select ALL the true statements.

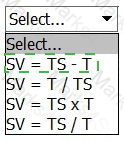

A time series (TS) is made up of two main components i.e. trend (T) and the seasonal variation (SV).

The equation that represents the seasonal variation under the additive model is:

MDS is facing a temporary shortage of Material H which is used to produce all three of its products.

In order to maximise its profitability, which product should be manufactured first?

A special contract requires 640 units of component T.

The inventory of 280 units of component T cost $0.20 per unit but the component is not currently used by the company.

The current market price of component T is $0.24 per unit but the inventory could be sold for $0.15 per unit.

The relevant cost of the units of component T required for the special contract is:

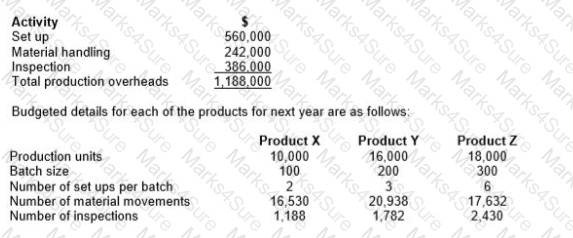

EF manufactures and sells three products, X, Y and Z. The following production overhead costs are budgeted for next year:

Required:

Calculate the total budgeted production overhead cost for each product using activity based budgeting.

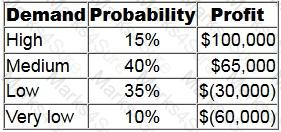

JDM is considering whether to go ahead with the launch of a new product. Profit from the new product is dependent on the level of demand.

The following table shows the estimated profits and their respective probabilities at different levels of demand.

The company could still cancel the launch of the product but would incur a cost of $7,000.

What is the maximum amount that the company should pay for perfect information about demand for the product?

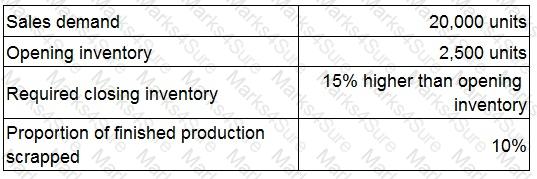

A manufacturing company is preparing the production budget for the forthcoming year.

The following budgeted information has already been obtained:

How many units will need to be produced for the forthcoming year?

Give your answer to the nearest whole number.

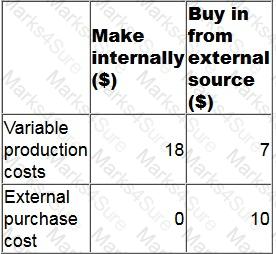

5c0e02ae-e691-41dd-b436-d41e2edaf83f: A company is using relevant costing to evaluate a make or buy decision.

The company already has a machine on an operating lease which can be used to make the product.

How would the lease rental cost be classified?

Information about a company ' s two products is as follows:

The products are currently sold in equal quantities.

Monthly fixed costs are $360,000.

What is the monthly breakeven sales revenue assuming a sales quantity mix of 50/50?

Give your answer to the nearest $.

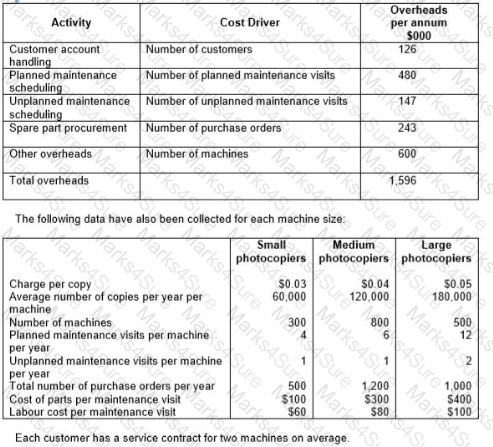

A company sells and services photocopying machines. Its sales department sells the machines and consumables, including ink and paper, and its service department provides an after sales service to its customers. The after sales service includes planned maintenance of the machine and repairs in the event of a machine breakdown. Service department customers are charged an amount per copy that differs depending on the size of the machine.

The company’s existing costing system uses a single overhead rate, based on total sales revenue from copy charges, to charge the cost of the Service Department’s support activities to each size of machine. The Service Manager has suggested that the copy charge should more accurately reflect the costs involved. The company’s accountant has decided to implement an activity-based costing system and has obtained the following information about the support activities of the service department:

Calculate the annual profit per machine for each of the three sizes of machine, using the current basis for charging the costs of support activities to machines.

Explain how probability analysis could be used to assess the risk of the evaluated projects.

Select all the true statements.

A company is bidding to win a special contract.

Which of the following is NOT a relevant cost to the company of undertaking the contract?

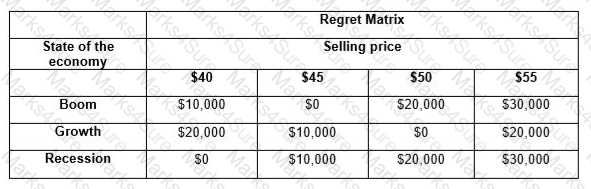

A marketing manager is trying to decide which of four potential selling prices to charge for a new product. The state of the economy is uncertain and may show signs of recession, growth or boom. The manager has prepared a regret matrix showing the regret for each of the possible outcomes depending on the decision made.

If the manager applies the minimax regret criterion to make decisions, which selling price would be chosen?

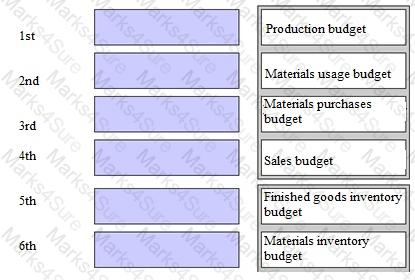

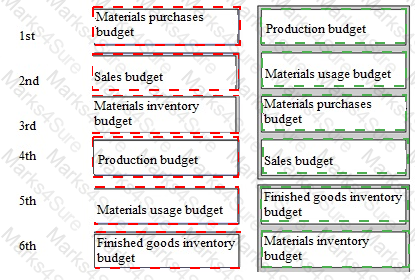

For a company that does not have any production resource limitations, what would be the correct sequence for budget preparation?

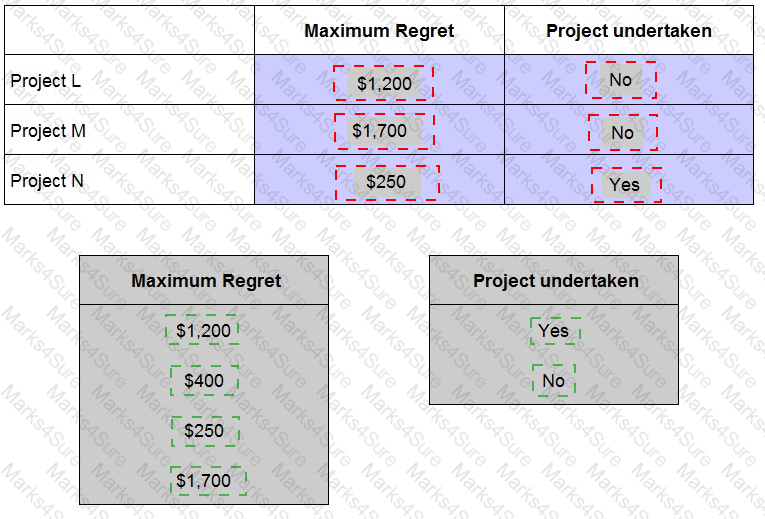

A company is choosing between three projects, Project L, Project M and Project N using minimax regret. The outcome from each project is dependent on competitor reaction. If this is passive returns will be L $4,000, M $3,500 and N $5,200. If it is aggressive returns will be L $3,200, M $2,800 and N $2,950. Place the tokens into the table to show the maximum regret for each project and whether the project would be undertaken using minimax regret.

A company manufactures three products X, Y and Z.

The company is currently operating at full capacity and is unable to meet the full sales demand for Product Z.

According to the latest management accounts, Product Y is loss making, whilst X and Z both make strong positive contributions.

Which of the following is relevant when making a decision on whether or not to discontinue the manufacture of Product Y?

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company’s planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company’s normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning.

The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

How will a manufacturing resource planning system improve the planning of purchases and production for the company?

Select ALL the correct answers.

A company makes a product using two materials, X and Y.

The standard materials required for one unit of the product are:

What is the direct material mix variance for Material X, using the individual valuation basis?

The maximum availability of a material is 8,000 kg.

Product A requires 5 kg of this material and Product B requires 7 kg of this material which is in short supply.

The correct constraint to include for the material when formulating the linear programming problem is:

A company has identified the trend in its sales figures through the regression equation Y = 65.9 + 3.86X, where Y is the sales revenue in thousands of dollars and X is the month number. The average seasonal variation for October is 87%

Calculate the forecast sales revenue for October of Year 6.

Give your answer to the nearest $000.

Sales volumes reported for the latest period are used by managers as the basis to forecast sales for the forthcoming period. The forecasts are compared with the budgeted sales and plans are adjusted to ensure that the budgeted sales are achieved.

This is an example of:

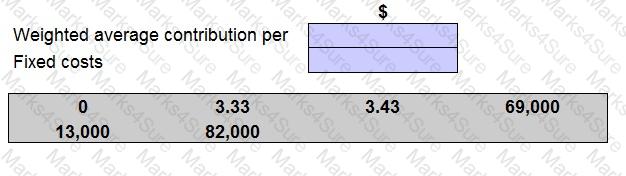

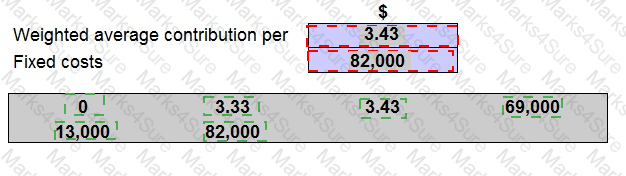

A company sells three products A, B and C in a ratio of 2:2:3.

Each unit of A,B and C earns a contribution of $4.00, $2.00 and $4.00 respectively. Production fixed costs are $69,000 each month and selling fixed costs are $13,000 each month.

The company holds no inventory. The management accountant wants to know the total number of units needed to break-even. However, he is unsure about how to calculate the weighted average contribution per unit or what category of fixed cost to use.

Place the amounts given to complete the table in order to calculate the total number of units to break even.

Company NBO is providing a quote to manufacture 500 passenger seats for a bus company.

Relevant cost is being used as the basis for the quote.

Which THREE of the following should be included as relevant costs or savings in the production of the 500 passenger seats?

A company accountant is trying to determine the optimum production plan for the period using linear programming.

The accountant has correctly formulated the linear programming problem as follows:

Variables (products): x and y

Objective function: Maximise contribution, C = 10x + 15y

Material constraint: 4x + 6y ≤ 500 (kg)

Labour constraint: x + 2y ≤ 350 (hours)

Machine constraint: 10x + 4y ≤ 1,500 (hours)

x constraint: 50 ≤ x ≤ 200

y constraint: y ≥ 0

Which of the following statements is true?

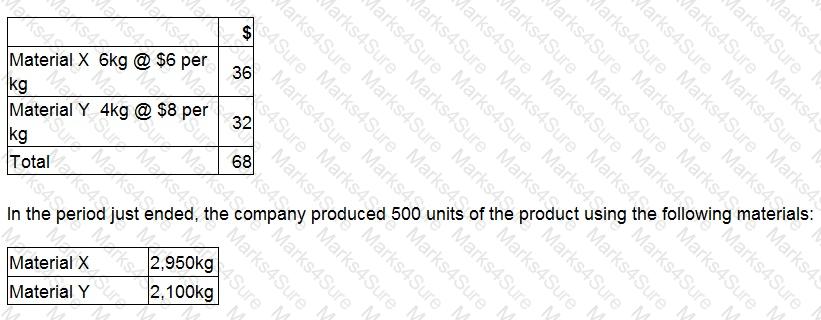

A company makes a product using two materials, X and Y.

The standard materials required for one unit of the product are:

What is the materials yield variance?

Give your answer as a whole number.

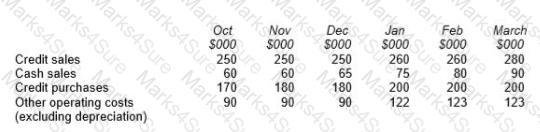

CH is a building supplies company that sells products to trade and private customers.

Budget data for each of the six months to March are given below:

80% of the value of credit sales is received in the month after sale, 10% two months after sale and 8% three months after sale. The balance is written off as a bad debt.

75% of the value of credit purchases is paid in the month after purchase and the remaining 25% is paid two months after purchase.

All other operating costs are paid in the month they are incurred.

CH has placed an order for four new forklift trucks that will cost $25,000 each. The scheduled payment date is in February.

The cash balance at 1 January is estimated to be $15,000.

Prepare a cash budget for each of the THREE months of January, February and March.

Select All the correct answers.

MBB is considering the costs to be incurred in respect of a special order.

The order would require 625 kg of Material K.

This is a material that is readily available and regularly used by the organization in its other products.

There are 265 kg of Material K in inventory which cost $1,590 when it was purchased.

The current market price is $6.48 per kg.

Material K is normally used to make Product X. Each unit of Material X requires 3 kg of Material K, and if Material K is costed at $6 per kg, each unit of Product X yields a contribution of $30.

The relevant cost of Material K to be included in the costing of the special order is:

A company ' s product has the following standard selling price, variable costs and contribution:

Budgeted sales and production was 20,000 units and actual was 19,500 units.

Due to a market downturn the production and sales budget should have been 10% lower.

What is the operational sales volume contribution variance?

Which THREE of the following are advantages of activity-based costing (ABC), in a multi-product environment, when compared with traditional absorption costing?

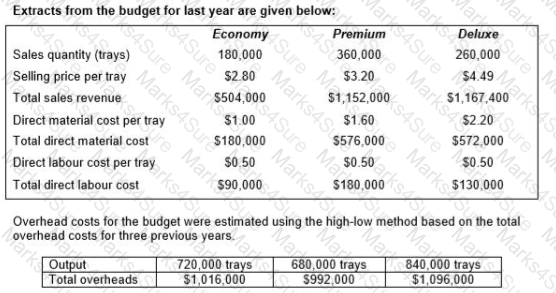

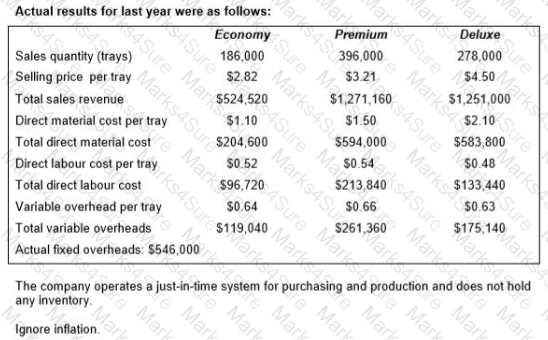

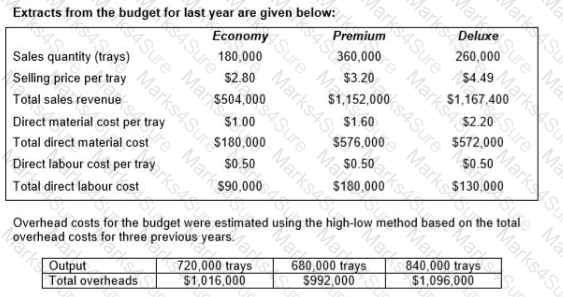

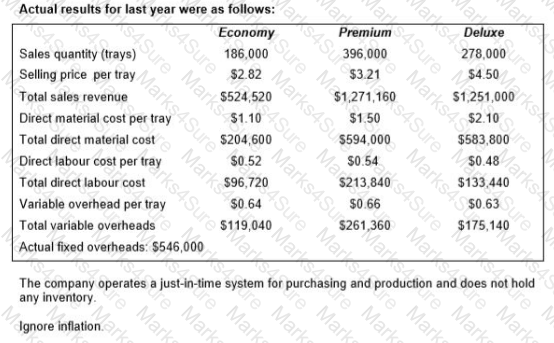

A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Calculate, for the original budget, the budgeted fixed overhead costs, the budgeted variable overhead cost per tray and the budgeted total overheads costs.

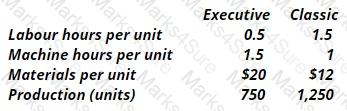

D3 makes 2 types of toilets - the Executive (Ex) and the Classic (CI). Direct labour costs $6 per hr and overheads are absorbed on a machine hour basis. The overhead absorption rate for the period is $28 per machine hour. What is the traditional cost per unit for (Ex) and (CI)?

JRL manufactures two products from different combinations of the same resources. Unit selling prices and unit cost details for each product are as follows:

Identify, using graphical linear programming, the weekly production schedule for products J and L that will maximize the profits of JRL during the next four weeks.

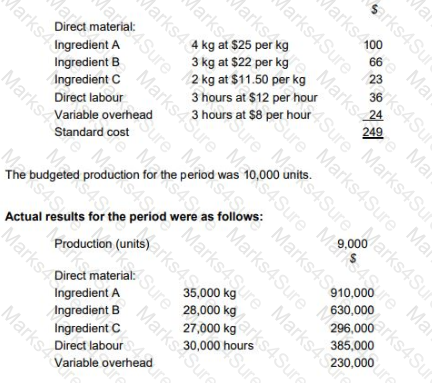

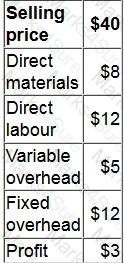

TP makes wedding cakes that are sold to specialist retail outlets which decorate the cakes according to the customers’ specific requirements. The standard cost per unit of its most popular cake is as follows:

The general market prices at the time of purchase for Ingredient A and Ingredient B were $23 per kg and $20 per kg respectively. TP operates a JIT purchasing system for ingredients and a JIT production system; therefore, there was no inventory during the period.

What was the material yield variance?

Company XPP sells a perishable product that has to be produced each day in anticipation of the following day ' s sales.

Any product remaining unsold at the end of the day following production is wasted.

The payoff table below shows the daily profit or loss depending on the amounts produced and sold.

A new ordering system is being discussed with customers.

The new system would require customers to order in advance to enable production each day of the following day ' s sales quantity, thus eliminating waste.

What is the expected increase in average daily profit if the new system is accepted by customers?

Give your answer as a whole number.

The breakeven point in units, in a multiple product context, is calculated using which of the following formulae?

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company’s planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company’s normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning. The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

What are the benefits for the company that could occur following the introduction of an activity based budgeting system?

Select ALL the correct answers.

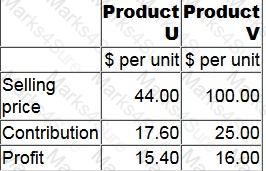

Information about a company ' s only two products is as follows:

The revenue from the products must be in the constant mix of 2U:3V. Budgeted monthly sales revenue is $110,000.

Fixed costs are $23,095 each month.

To the nearest $10, what is the budgeted monthly margin of safety in terms of sales revenue?

Since there is no likelihood of them receiving a pay rise in the foreseeable future, your colleagues are considering leaving their current employment and starting their own business.

When preparing the data to evaluate their decision, their current salaries would be:

You are a trainee management accountant working for a prestigious manufacturing firm. One day you go to a business meeting a business meeting and the managing director is there. They stand up and say that the

company is losing too much money through wastage and losses and so they have decided to implement a total quality management system. They go on to say this system will:

1:Allow the company to improve on a consistent and continual basis

2:Allow the company to identify and allocate quality accountability to certain departments

3:Help the company detect error and fraud

Are ALL of these statements correct?

A manufacturing company produces and sells a single product.

It is preparing its budget for the next period and expects to breakeven.

Budgeted fixed costs are the same as budgeted variable costs and the budgeted contribution to sales ratio is 50%.

If all budgeted costs decreased by 10%, which of the following statements is true?

A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Discuss the benefits of flexible budgeting for planning and control purposes.

Select all the true statements.

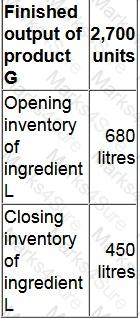

Each finished unit of product G contains 2 litres of ingredient L. Losses during production are 10% of input of ingredient L. Budgeted data for next period are as follows:

The budgeted purchases of ingredient L for next period are:

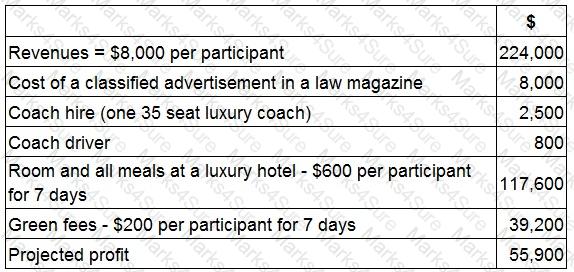

JKI is planning a golfing holiday for a group of wealthy lawyers.

The lawyers will fly to the local airport at their own expense. JKI will then pay for transport, accommodation and the use of the golf course (green fees).

JKI ' s costings are as follows, based on 28 participants:

JKI received 46 applications from potential participants.

What would the profit be if JKI accepted all of these bookings?

Give your answer to the nearest whole number.

Traditional absorption costing is more suitable than activity-based costing when:

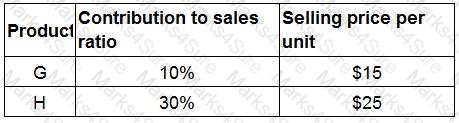

XY sells two products for which the budgeted contribution to sales ratios are as follows:

Total budgeted sales revenue is $920,000, of which $368,000 will be generated by product X. The products must be sold in a constant mix.

Budgeted fixed costs are $105,000.

What is the budgeted breakeven sales revenue?

Give your answer to the nearest $.

A company manufactures a range of products. It is deciding whether to make one of its products internally or to buy the product partially completed from an external source and complete the manufacture in-house. The table below gives details of the variable costs of the two alternatives. Fixed production costs will remain the same under both alternative.

What is the sensitivity of the decision to a change in the external purchase price?

Give your answer as a whole percentage.

The budgeted production of product G for the period was 300 units. At the end of the period it was discovered that the standard hourly rate for labour should have been higher than that originally planned. Actual production was 450 units.

The labour rate planning variance would be calculated as:

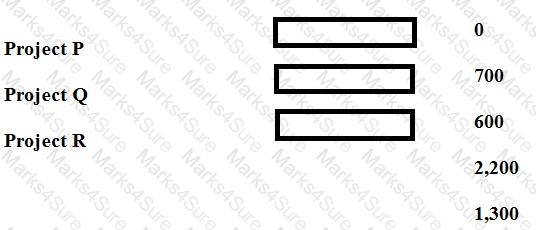

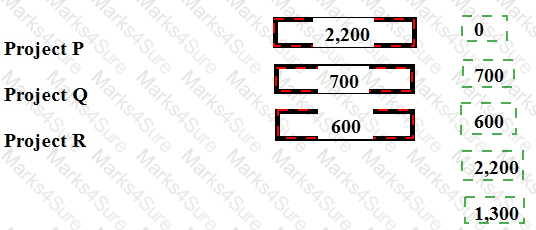

A company is choosing between three projects, Project P, Project Q and Project R using minimax regret as the criterion for the decision. The outcome from each project is dependent on future economic growth. If this is strong, returns will be P $5,000, Q $6,500 and R $7,200. If it is weak, returns will be P $3,500, Q $4,800 and R $4,200.

Place the correct figures into the table to show the maximum regret for each project.

Which THREE of the following are never relevant costs for short-term decision making?

When a moving average is plotted onto a graph, where should the plotted points be located?

A company is considering whether to launch a new product. The selling price and costs for each unit of the product are shown in table below:

The fixed overhead cost is based on expected production of 2,000 units.

The company will only launch the product if it is expected to be profitable.

To which of the following is the decision to launch the product most sensitive?

A company operates a customer complaints department.

How will the cost of the customer complaints department be classified in a system focussed on quality related costs?

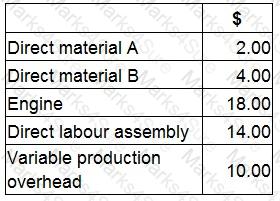

A company manufactures a machine. The machine is made from two types of raw material and is assembled in a factory using skilled labour. The engine for the machine is purchased from an outside supplier.

The following costs relate to the manufacture of one machine:

What is the finished goods inventory valuation for one machine using throughput costing?

Assume that you have made profit calculations based on standard profit calculation methods and activity based costing methods.

In which ways will this information be beneficial to the management team?

Select all the true statements.

Which costing method, used in just-in-time (JIT) production systems, attaches cost directly to output rather than following the flow of product through the production process?

The labour requirement for a special contract is 250 skilled labour hours paid at $10 per hour and 750 semi-skilled labour hours paid at $8 per hour.

At present, skilled labour is fully utilised on other contracts which generate a $12 contribution per hour, after charging labour costs. Additional skilled labour is unavailable in the short term.

There is a surplus of 1,200 semi-skilled hours over the period of the contract but the firm has a policy of no redundancies.

The relevant cost of labour for the special contract is:

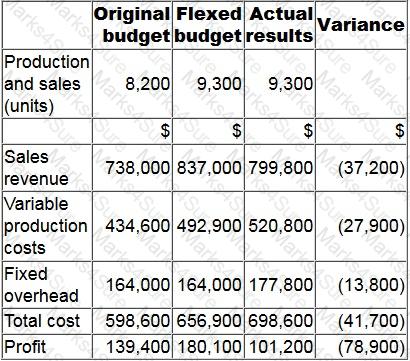

The budgetary control report of XYZ for the latest period is shown below. Variances in brackets are adverse.

What is the sales volume profit variance?

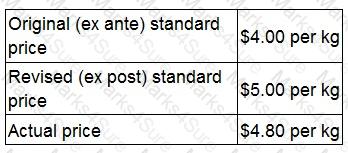

A company reports planning and operational variances to its managers. The following data are available concerning the price of direct material M in the last period. Material M is the only material used by the company. The company operates a just-in-time (JIT) purchasing system.

Which TWO of the following statements about last period are definitely correct based on this information?

The direct material price operational variance was adverse.

When classifying quality costs, which of the following is NOT likely to be an appraisal cost?

RFT, an engineering company, has been asked to provide a quotation for a contract to build a new engine. The potential customer is not a current customer of RFT, but the directors of RFT are keen to try and win the contract as they believe that this may lead to more contracts in the future. As a result, they intend pricing the contract using relevant costs. The following information has been obtained from a two-hour meeting that the Production Director of RFT had with the potential customer. The Production Director is paid an annual salary equivalent to $1,200 per 8-hour day. 110 square meters of material A will be required. This is a material that is regularly used by RFT and there are 200 square meters currently in inventory. These were bought at a cost of $12 per square meter. They have a resale value of $10.50 per square meter and their current replacement cost is $12.50 per square meter. 30 liters of material B will be required. This material will have to be purchased for the contract because it is not otherwise used by RFT. The minimum order quantity from the supplier is 40 liters at a cost of $9 per liter. RFT does not expect to have any use for any of this material that remains after this contract is completed. 60 components will be required. These will be purchased from HY. The purchase price is $50 per component. A total of 235 direct labour hours will be required. The current wage rate for the appropriate grade of direct labour is $11 per hour. Currently RFT has 75 direct labour hours of spare capacity at this grade that is being paid under a guaranteed wage agreement. The additional hours would need to be obtained by either (i) overtime at a total cost of $14 per hour; or (ii) recruiting temporary staff at a cost of $12 per hour. However, if temporary staff are used they will not be as experienced as RFT’s existing workers and will require 10 hours supervision by an existing supervisor who would be paid overtime at a cost of $18 per hour for this work. 25 machine hours will be required. The machine to be used is already leased for a weekly leasing cost of $600. It has a capacity of 40 hours per week. The machine has sufficient available capacity for the contract to be completed. The variable running cost of the machine is $7 per hour. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour.

Select ALL the true statements.

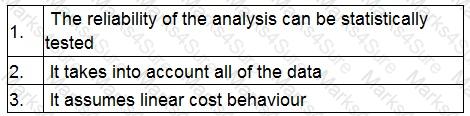

The following statements relate to the advantage(s) that linear regression has over the high-low method in the analysis of cost behaviour:

Which statement(s) is/are true?

Which of the following are examples of feedforward control?

Select ALL that apply.

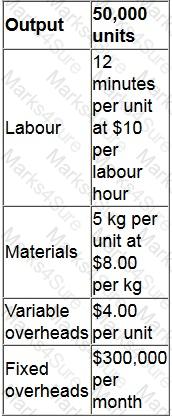

A company ' s budgeted data for the period are shown in the table below.

There is a stepped increase in fixed overheads of $10,000 when production exceeds 52,000 units.

Actual production for the period was 60,000 units.

What is the flexed budgeted cost for the period?

Give your answer as a whole number (in ' 000s).

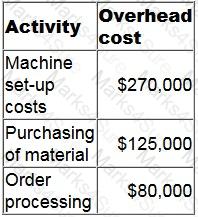

PQR has recently introduced an activity-based costing system.

It manufactures three products, details of which are given below.

The budgeted production overhead costs for the year are shown in table below:

What is budgeted machine set-up cost per unit of Product J?

Give your answer to the nearest cent.

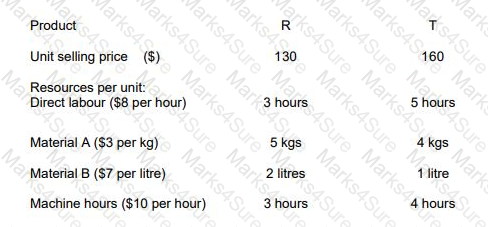

RT produces two products from different quantities of the same resources using a just-in-time (JIT) production system. The selling price and resource requirements of each of the products are shown below:

Market research shows that the maximum demand for products R and T during June 2010 is 500 units and 800 units respectively. This does not include an order that RT has agreed with a commercial customer for the supply of 250 units of R and 350 units of T at selling prices of $100 and $135 per unit respectively. Although the customer will accept part of the order, failure by RT to deliver the order in full by the end of June will cause RT to incur a $10,000 financial penalty. At a recent meeting of the purchasing and production managers to discuss the production plans of RT for June, the following resource restrictions for June were identified: Direct labour hours 7,500 hours

Material A 8,500 kgs

Material B 3,000 litres

Machine hours 7,500 hours

Assuming that RT completes the order with the commercial customer, prepare calculations to show, from a financial perspective, the optimum production plan for June 2010 and the contribution that would result from adopting this plan.

The contribution per unit for R and T will be...?

PDF + Testing Engine

Testing Engine

PDF (Q&A)